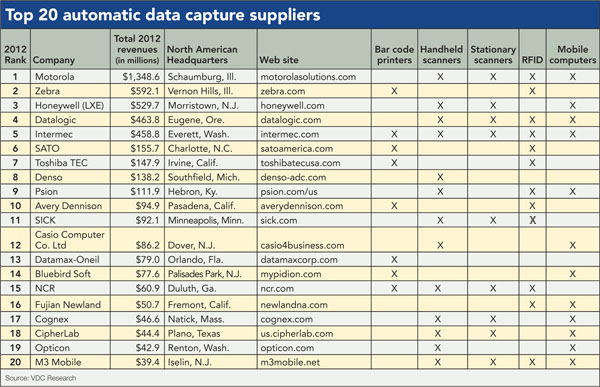

Top 20 Automatic data collection suppliers

The ADC market grew incrementally in 2012 amid changing customer interests and stiff competition.

Latest Logistics News

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report More NewsLast year, the global market for automatic data capture solutions (ADC) used in factories, warehouses and logistics applications reached $11.264 billion in sales, according to VDC Research Group.

The ADC market includes handheld and stationary bar code scanning and imaging devices, bar code printers, RFID solutions for the supply chain and ruggedized mobile computing solutions for the factory and warehouse.

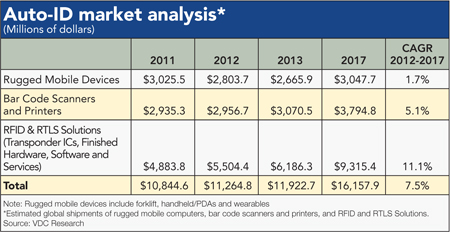

The global sales figures represent a 3.9% increase from 2011’s comparable estimate of $10.884 billion, which was revised down slightly from what Modern reported last year. The revisions were due to improved vendor reporting and VDC data validation efforts and do not reflect any changes in the market, according to Michael Liard, VDC’s vice president of Auto-ID. But while the market as a whole continues to climb steadily upward, a look into individual segments reveals changing dynamics. Examples include the market for industrial printers, which declined by more than 2% as a result of tough competition from vendors in the emerging markets, a 7% drop in rugged mobile devices and a nearly 13% jump in the market for RFID solutions.

The 2012 market leaders included familiar faces. Once again, Motorola Solutions topped the chart with an estimated $1.348 billion in revenue. Zebra Technologies again placed second with $592 million. The top five was rounded out by Honeywell, which took the No. 3 spot with $529 million; Datalogic, which claimed No. 4 with $463.8 million; and Intermec, which dropped one place on the chart with $458.8 million. (Read last year’s Top 20 ADC supplier list.)

Going forward, Liard and his colleagues anticipate sustained growth as a result of new customer interests, increased competition and opportunities in emerging markets. VDC is projecting a compound annual growth rate (CAGR) of 7.5% through 2017 for the overall industry, when combined revenues are expected to reach $16.158 billion.

In addition, Liard expects to see the continued hybridization of multiple data collection technologies as a key driver of growth. “More and more we are seeing the silos collapse,” he says. “Both vendors and end-users are looking at business problems, operational inefficiencies and what can address them, whether RFID or bar code.” In addition, companies are looking to reduce the number of vendors involved in providing those solutions, he adds.

That notion is reflected in the continuing consolidation of suppliers. Next year, following the recent completion of Honeywell’s acquisition of Intermec, the jointly reported numbers could position Honeywell in second place. Next year will also reflect Motorola’s acquisition of Psion. Other notable changes from last year’s list include an adjustment of Avery Dennison’s overstated revenues for 2011, although it again claimed 10th place.

Collecting the data

This is Modern’s 12th-annual look at the leading manufacturers of ADC hardware and solutions. Because the industry includes public and private companies, this is the fifth year in a row that VDC Research Group compiled our data—since they are covering this technology every day, they are closest to this market.

To make our list, companies must sell in North America, though the chart includes worldwide revenues. Modern does not include resellers, systems integrators or other companies that do not manufacture ADC hardware. Since our readers are primarily focused on supply chain solutions, we do not include companies whose primary focus is the retail checkout counter or non-industrial settings like hospitals, libraries or resorts. Nor do we include companies that only manufacture consumables like bar code labels and RFID tags.

Market by market

The Auto-ID market is made up of three distinct industry segments, each with its own distinct dynamics—mobile computing, scanning and printing, and RFID. Here are the most important developments in each market.

Mobile computing: The market for ruggedized mobile computers reached $2.803 billion in 2012, says David Krebs, vice president of VDC’s enterprise mobility and connected devices. Those figures include handheld/PDA devices, wearable mobile computers and lift truck-mounted devices used on the plant or DC shop floor or in port and yard applications.

Krebs estimates the overall market for mobile computing devices will grow by a CAGR of 1.7%, reaching about $3 billion by 2017. As with 2011, transportation and warehousing continued to drive investment in mobile computing. And, while 2012 saw a continuation of the recovery that started in 2010, Krebs is expecting some changes in 2013.

“The rugged handheld market is in the midst of a fair amount of change,” says Krebs, who says market conditions have not been good from a top line perspective. “We saw contraction last year and expect it again this year.” One factor is macroeconomic, such as struggling European markets that have caused some tension in terms of investment strategies, Krebs says.

The second factor is technical, with disruption in industrial mobile computing increasingly defined by consumer-grade equivalents. “These technologies find their way into an enterprise through the back door, with things like ‘bring your own device’ programs. Enterprise-deployed programs, while they do happen, are not the norm,” Krebs says. The availability of consumer products makes it difficult for traditional rugged vendors to compete, but the lack of support tools is leading to decreased acceptance of consumer devices for enterprise-level data access. “The pain threshold is also difficult to overcome in the event of failure of these consumer devices,” Krebs says. “At the end of the day, customers want something as reliable as possible, and that’s a premium the market is willing to pay for.”

When it comes to operating systems, the mobile computing market is for the most part owned by Microsoft, especially in the warehouse and logistics space. However, with the introduction of Windows 8, there are questions as to whether that will create opportunities for alternative operating systems, Krebs says. “If a company is upgrading its hardware, it may look into other options available on the market,” he says. “Microsoft is struggling in terms of mobile strategy. You see the results of that in the mobile market.”

Krebs is watching a few key trends:

- Multi-modal solutions, such as the combination of voice and bar code scanning or voice and light-directed picking, continue to gain steam as companies grapple with how to fill e-commerce orders accurately and efficiently. “As greater volumes of orders are fulfilled through electronic channels and as retailers look to provide customers with more options, the need for warehouse and logistics functions has to change,” he says. “We’ve seen this most acutely in the drive toward the perfect order as a key metric of performance. We see integration and deployment of multiple types of data collection technology to support those more stringent metrics.”

- Form factors are also changing in the mobile market, as wearable technologies become more accepted and as interfaces migrate from keystroke-intensive approaches to touch-based designs. “We see the influence of consumer technologies in warehouse environments, including the design of both hardware and applications around touch as an input methodology,” Krebs says.

- Wearable, intuitive systems facilitate a greater emphasis on efficiency in the warehouse. “An improved process is one thing, but labor management and the efficient, on-the-fly redeployment of labor is also key,” Krebs says.

Scanning and printing: Although market totals remain virtually unchanged in 2012, the totals reflect a significant uptick in the number of customers migrating from scanning to camera-based imaging, particularly on the handheld side.

“The transition has been much faster than expected,” says Richa Gupta, the VDC senior analyst for the Auto-ID market. Although camera-based imaging technology has been around for more than 10 years, it was not until recently that the prices fell to more appealing levels. “Many leading vendors were not expecting customers to switch as fast as they did,” says Gupta. “Laser scanners are on the decline and will continue to be. Camera-based imaging solutions are the future.”

As with 2011, camera-based 2D imaging solutions saw the largest area of growth, expanding by more than 30%. That growth is largely being driven by retail markets, where functionality such as scanning a bar code from a customer’s smart phone is becoming increasingly important.

Handheld scanners jumped nearly 7% to $945 million, while the market for industrial fixed scanners increased by just 1% to $675 million, according to Gupta. Meanwhile, the market for industrial printers, which includes bar code printers and the RFID printer/encoder market, declined more than 2% to $1.33 billion. However, Gupta sees growth returning, projecting a five-year CAGR of 5.1%.

On the printing side, there is a lot of commoditization, Gupta says. “There are so many vendors to choose from, and the market is getting increasingly fragmented,” she says. “Vendors are struggling to hold onto customers while facing very stiff competition from Asia, given the low barriers to entry due to the plug-and-play nature of these solutions.”

While camera-based technologies represent a new market for vendors to expand into, there are no new and emerging printing technologies with which vendors can differentiate themselves. “They’re competing for the same set of customers with the same product portfolio,” she says. “If anything, most of the innovation is coming on the mobile printer front.”

Mobile printing saw a double-digit jump from 2011 to 2012, while the rest of the market stayed relatively flat. Overall, the Americas were one region that did very well, driven by mobile printer investments. Asia-Pacific declined while Europe also struggled with an ongoing financial crisis and manufacturing slowdown.

On the stationary scanning side, a surprising decline was recorded across product categories. Point-of-sale scanners stayed relatively flat, but Gupta says we can expect the overall stationary scanning market to pick up in 2014. “Camera-based technologies are making huge gains in the handheld market, but are only just now creeping into the stationary point-of-sale space.”

Vendors are also looking to grow their presence in emerging markets in Asia. As a result, although vendors like Motorola, Honeywell and Datalogic might not shift much in 2013 or 2014, Gupta suspects they will increasingly focus their efforts on emerging markets. Zebra is still No. 1 on the bar code printing side, for instance, but faces stiff competition from Chinese and Taiwanese manufacturers, who are also looking to expand their presence in emerging markets.

RFID: After growing by double-digit rates in 2011, the RFID market again grew nearly 13% from $4.8 billion to $5.5 billion in 2012. Looking forward, the market is expected to post a CAGR of 11.1% through 2017, according to Liard.

Since last year, RFID has become further entrenched in apparel handling. Liard says RFID in apparel has reached the tipping point, with several billion RFID tags sold in 2012 as compared to the low hundreds of millions in prior years. As more stores become RFID-enabled, more retailers are supporting item-level RFID, Liard says. “In retail apparel, we see additional product lines being included under the umbrella of RFID,” he says. “Where previously they were focused almost exclusively on apparel, they’re now looking at tagging more products.”

RFID is part of the multi-channel conversation, he says. “Customers are looking at how to turn stores into miniature distribution centers and use RFID not only for inventory control but for shipping and receiving operations.”

Increased interest is also apparent in applying RFID tags closer to the point of manufacture. “Some do it in the DC, some in the back room of a retail store, and some at point of manufacture,” says Liard. “But when you talk about multi-channel, you need that visibility through the entire supply chain.”

Last year, Liard anticipated growth in RFID being used for asset management, which also continues to progress. “Aside from transportation, logistics and manufacturing, it’s reaching some of the non-traditional industries, from oil and gas to construction and mining, and increasingly in health care,” he says.

As it becomes further embedded in traditional applications, RFID technology is also innovating to accommodate a growing number of asset and product types. “Whether hardware or form factors for tags and readers, innovation continues unabated in RFID,” Liard says. “For 2014 and beyond, I’m interested to see what will happen with embedded RFID solutions in kiosks and consumer electronics. The volume of units is trending in the direction of embedded opportunities, as opposed to traditional handheld and fixed position readers.”

As a result, Liard says he continues to see new players enter the market, with continued investment in RFID-focused firms. “Players are still coming out of China both for readers and tags,” he says, “after many years of being dominated by North America and Europe.”

Article Topics

Latest in Logistics

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report XPO opens up three new services acquired through auction of Yellow’s properties and assets More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources