Top 50 Trucking Companies: Tough at the top

Analysts and top trucking executives agree that a sharp focus on a durable business plan and dependable operations are vital to remaining profitable in one of the most challenging trucking environments in history.

Latest Logistics News

Warehouse/DC Automation & Technology: It’s “go time” for investment 31st Annual Study of Logistics and Transportation Trends Warehouse/DC equipment survey: It’s “go time” for investment Global Logistics/3PL Special Digital Issue 2022 Motor Freight 2022: Pedal to the Metal More Special ReportsAt its essence, trucking sounds so simple: Find a niche, create a business plan, execute it on a daily basis, eliminate exceptions, charge decent rates, and then get paid. However, those executives leading the biggest and most profitable trucking companies will tell you that executing this theoretically straightforward plan every day is anything but.

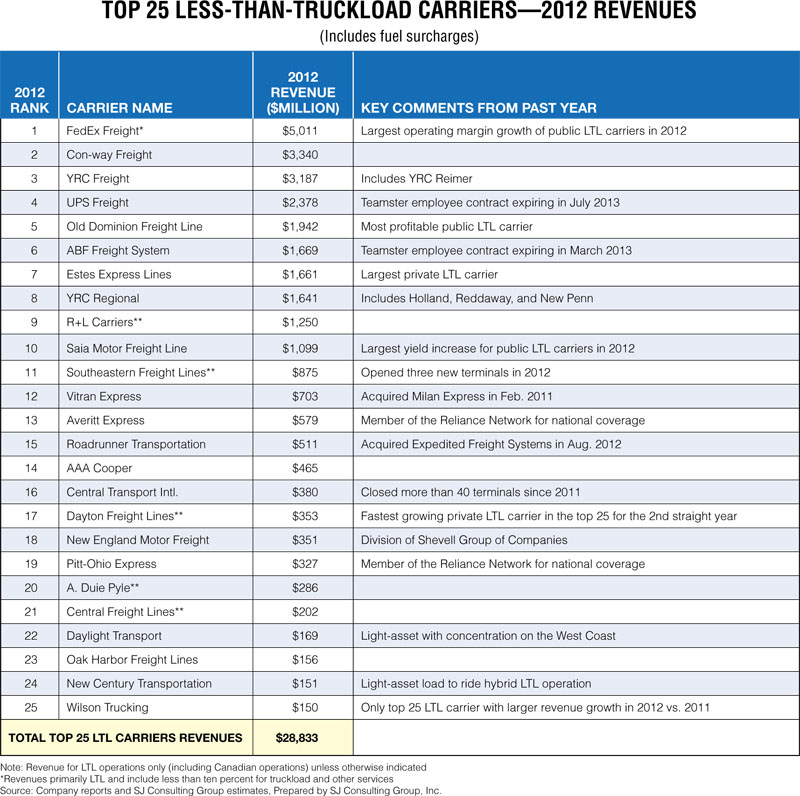

“For us, I think a lot of it goes back to the strategic planning we did 15 years ago,” says David Congdon, president and CEO of Old Dominion Freight Line (ODFL), No. 5 on Logistics Management’s (LM) Top 25 LTL listing and one of the most profitable LTL carriers in the country. Congdon says that the path to ODFL’s current perch was long and involved and could have only been achieved by staying focused on core business principals that are paying off now.

Analysts and top trucking executives agree that a sharp focus on executing a sound business plan is one of the keys to making the list of Top 50 Trucking Companies. The other elements, say our top sources, would be attention to detail, employee relations (both union and non-union), financial strength, information technology, and operational execution.

“Trucking is not a business where money just rolls through the door.” says Donald Broughton, trucking analyst with Avondale Partners. “Everybody knows what they need to do: lower empty miles, minimize fuel, maximize revenue per truck. But execution is hard, and it’s tough to establish the discipline every day to force your customers, suppliers, and employees to do that. It requires a lot of work and thousands and thousands of hours of planning.”

Mike Shevell, chairman of the Shevell Group that includes New England Motor Freight (No. 18 on the LM LTL list), says that the key to success is getting proper rates to haul freight. “Without rates that can give us proper profit, there’s going to be a very serious problem in future,” he says. “Our cost of doing business is off the charts, and regulations are putting a noose around our neck. It’s getting more difficult to operate.”

Despite the most brutal operating environment in years, the top carriers on our lists are managing to stay focused on service. There’s an old saying in trucking that “you get the business on price, but you keep it on service.” Executives and analysts agree.

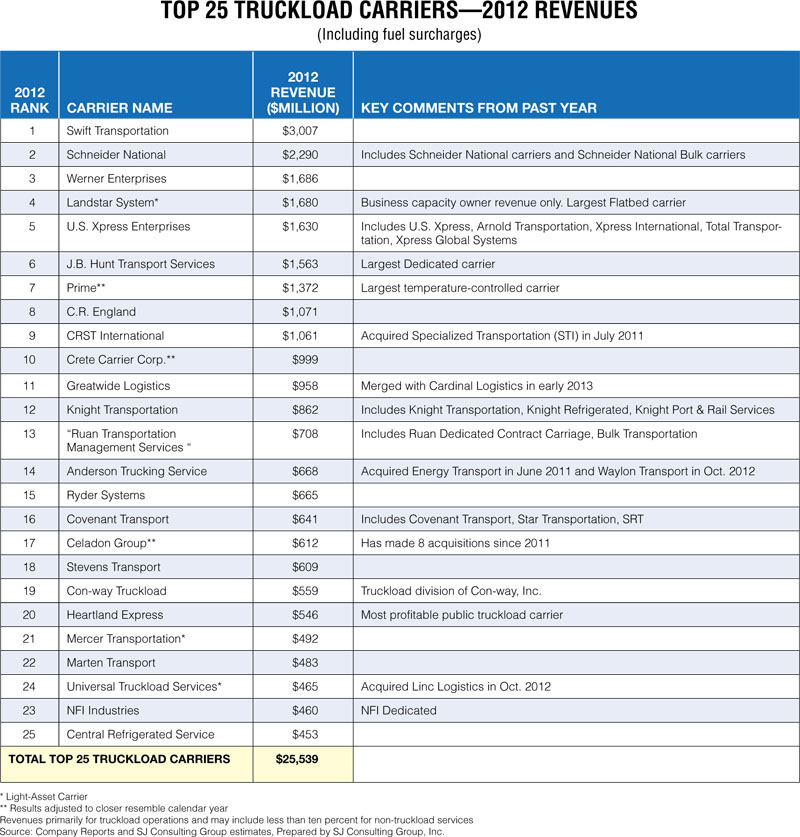

“You prove yourself to customers in a tight environment where there’s very little capacity,” says Saul Gonzalez, president of Con-way Truckload (No. 19 on the LM TL list). Gonzalez is quick to credit his employees as the key differentiators. “Our employees are what separate us. They strive to make us better.”

During a recent conference call with analysts and investors after another solid financial quarter, ODFL’s Congdon was asked how his trucking company was able to obtain such strong freight rates. Congdon’s answer was nothing less than direct: “We’ve found that it’s a lot easier to sell a service equation, if you have it. In order to get paid for good service, you have to offer good service.”

To ensure good service, Con-way’s Gonzalez says that he makes sure to talk to every new driver. “It’s my job to communicate how to represent Con-way as a professional. How they dress, how they pick up and deliver, how they interact with customers. It’s important that they know that from the first day, and I do that personally.”

That attention to detail may be one of the key common denominators among all members of the LM Top 50. Deregulation weeded out the poor operators in trucking, and those now toward to top all execute terrific service. Here are a few of the back stories on how some of the Top 50 are able to maintain their position year after year.

Staying on top

About 20 years ago, Old Dominion Freight Line was nearly exclusively a Southeast regional carrier, competing with a host of other top-flight, mostly non-union carriers offering nearly identical next- and second-day LTL service. Congdon, who was then working under his father Earl the CEO, realized ODFL had to diversify.

“We spent lot of time building a portfolio of service that works together with our technology, and that touches everything we do,” says David Congdon. “But we had to stay focused on the basics, and that’s the key thing.”

Today, ODFL offers regional, inter-regional, and intrastate domestic shipping, assembly and distribution, domestic drayage, direct service to Canada, and even full container load ocean carriage. Two-thirds of its trucking business is two-day or less with 86 percent third day or less.

“We have a very good blend of regional, interregional, and long-haul across our network,” Condon explains.

ODFL earned $169 million net income on $2.1 billion revenue last year as the most profitable LTL carrier in the land. It’s operating ratio (OR) was an eye-popping 86.5, and that came on top of an 87.6 OR in 2011 and 90.7 in 2010—by far the lowest three-year OR in the LTL sector. “We’re not perfect by any stretch,” adds Congdon. “But we’ve got it honed down pretty well so we can balance pricing and network growth and customers and so forth. We’ve got a good balance of proper things going on.”

At the opposite end of the LTL profit spectrum is ABF Freight System, the nation’s seventh largest LTL carrier. Hurricane Sandy and a continued weak freight environment were two conspirators that created a 2012 income loss of $7.7 million at parent Arkansas Best Corp.—a swing of almost $14 million when compared to the $6.159 million net income in 2011. Revenue remained steady at just over $2 billion annually.

ABF (No. 6 on the LM LTL list) is currently in crucial labor talks with the Teamsters union that will likely prove decisive in whether it will be profitable going forward. The company is now asking for concessions like those obtained by YRC Worldwide (No. 3 on the LM LTL list).

YRC may be the poster child for trucking turnarounds. After losing in excess of $2.6 billion from 2006 to 2011, YRC turned an operating profit last year. It changed its management team, installing former YRC executive James Welch to replace Bill Zollars as CEO—and the move has paid off.

In a recent conference call with investors, Welch resisted the urge to run YRC’s operating profit up the flagpole. That was a small battle, he said. The war has yet to be won.

In one of his most important early moves, Welch installed Jeff Rogers as president of YRC Freight, its long-haul and largest subsidiary. Rogers is a “blocking-and-tackling” fanatic with a knack for employee relations. In a recent letter to YRC Freight employees, Rogers told his workers that they indeed accomplished a lot in turning around the company—but much more remains.

“There’s no doubt about it, we’re getting our swagger back,” wrote Rogers in the letter. “Here comes the honest truth, though: All our recent successes won’t mean a thing unless we deliver results in 2013. We simply must win in the marketplace, and I mean now. This is the year we go from survive to thrive.”

Managing the issues

The best trucking executives say that there are many paths to success, but they all stress that there can be no shortcuts in service.

John White, executive vice president of sales and marketing for U.S. Xpress, the nation’s second largest privately held TL, says that the most important thing is to be relentless on deciding what’s best for shippers. “If we focus on making our customers better, we’re going to be successful,” White says.

Yet White adds that trucking is more complicated than that, even the most serious senior leadership team that’s focused on customers. That’s because of what White called the “murky horizon,” which includes an uncertain supply of drivers, rising equipment costs, and an unclear legislative landscape that might include reduced hours of service and other productivity cuts

“It’s hard to plan and work the plan for five years,” says White. “The challenge moving forward is moving purely away from being an entrepreneurial spirit to being a little more disciplined. You have to be in front on some challenges.”

The issue of onboard electronic recorders (EOBRs)—the so-called black boxes—is a good example. Washington recently mandated EOBRs for all new trucks, probably starting with the 2015 model year. Sensing this inevitable move, U.S. Xpress began installing the boxes several years ago and will soon have its entire fleet outfitted.

“We knew that was coming,” says White. “EOBRs will help our drivers better understand time management, and it will help us manage our business better as the legislative landscape evolves.”

If hours-of-service rules change, the data captured by those EOBRs will be invaluable in creating new lane and truck assignments, White adds. In short, a little advance preparation will help smooth what could be a rocky transition for others.

Offering new services is another way to stay on top. U.S. Xpress recently launched a new refrigerated service offering to its grocery customers that wanted to improve shelf life of some produce. “We’re constantly being asked to bring innovation into the market place,” says White, adding that the service now involves 150 trucks.

The Shevell Group’s Eastern Freightways TL unit has grown its dedicated and flatbed business in recent years due to customer demand. “Our flatbed business has mushroomed,” says Shevell. “It’s been a huge success, and we feel it will be even better as construction rebounds through the economy. If the economy grows, that will grow.”

Other carriers have started new services to attract shippers. As an example, Con-way Truckload recently began offering double-stack trailers that can adjust the interior height to increase available payload. Some pallets can’t be stacked because of weight and configuration; however, these double-stack trailers can adjust the height of the floor so more freight can be hauled. “That’s been really helpful to us,” Gonzalez adds.

Costs skyrocketing

All trucking executives interviewed for this story say that the cost of doing business is rising at least 10 percent a year. Trucks that cost $80,000 five years ago are now $125,000. Fuel is staying stubbornly near $4 a gallon, while drivers remain scarce and are costing more than ever to train and retain.

“The cost of everything is going up—terminals, equipment, insurance, fuel, trucks, drivers,” says Shevell. “And the driver shortage is only going to accelerate as the economy comes back.” And after examining the new health care act, Shevell concludes that its costs will be “mind-boggling” to carriers. “It’s going to hurt carriers’ profitability,” he says. “It’s been bad enough the last five years, but with everything going up, there are not enough pennies around our neck to pay for it.”

For shippers that will mean rate increases in the low- to mid-single digits, perhaps more on lanes where capacity is extra tight. “The industry is not earning enough to sustain itself in order to continue on a successful basis,” says Shevell. “Notwithstanding the driver shortage, once the business demand exceeds capacity, you’re going to see a very serious problem, and when it comes is anybody’s guess. But, it’s going to happen.”

That will mean that those carriers with sufficient financial stability will be able to obtain the credit necessary to purchase or lease new trucks. Those without…well, who knows.

“Some carriers’ financial stability is wonderful, and some I wonder how they do the things they do,” says Shevell. “We’ve just spent $25 million for new equipment this year and we’ll spend another $10 million before the end of year. If carriers don’t continue to re-power their fleets, I don’t know how they’re going to be able to survive.”

The key to survival is deciding how to anticipate shipper needs. “We all have an obligation of creating value,” says Dan Van Alstine, senior vice president and general manager of dedicated services at Schneider National (No. 2 on the LM TL list). “But the successful companies are creating value for customers, shareholders, driver associates, and for the communities in which we operate. It’s a cliché, but it’s true.”

White of U.S. Xpress says that his customers are asking more than ever how they can differentiate themselves through supply chain excellence by driving excess inventory and eliminating costs from their systems. But this more strategic approach will cost shippers through rising rates, he says.

“We can strategically work with our customers to drive improvement and mitigate issues,” adds White. “But invariably, we’re going to see continued pressure on price in base truckload rates. Whether it’s HOS, equipment, cost of drug testing, sleep apnea testing…those are all positive and important things and will continue to improve safety and environment. But all those things come with a cost. You will continue to see upward pressure on price.”

Ideally, carriers hope to form long-term strategic relationships with customers instead of what White termed “tactical ones.” However, White says he believes that at the end of the day prices will continue to escalate.

In the truckload sector, the largest TL carrier, Swift Transportation, has less than 2 percent market share. In such a fragmented market, gaining pricing power is difficult. But that doesn’t mean TL carriers aren’t getting more strategic with rates. “Capacity hasn’t been expanding, so we’ve seen the industry gain some discipline,” White adds. Going forward, some carriers may want to expand the asset-light side of their business through brokerage or 3PL services while eschewing large capital expenditures to buy assets outright.

J.B. Hunt (No. 6 on the LM TL list) is an excellent example of that. Its intermodal business grew 13 percent last year while its pure truck business continued to shrink, showing a 27 percent decline in operating income. Shippers can expect Hunt’s Truck division to continue to shrink and receive little additional capital as Hunt continues to find greater return on investment in other units.

All that reduction in over-the-road capacity will do over time, analysts and executives say, is push up trucking rates for the rest of the industry.

Article Topics

Special Reports News & Resources

Warehouse/DC Automation & Technology: It’s “go time” for investment 31st Annual Study of Logistics and Transportation Trends Warehouse/DC equipment survey: It’s “go time” for investment Global Logistics/3PL Special Digital Issue 2022 Motor Freight 2022: Pedal to the Metal Top 50 Trucking Companies: The strong get stronger 2019 Top 50 Trucking Companies: Working to Stay on Top More Special ReportsLatest in Logistics

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Warehouse/DC Automation & Technology: Time to gain a competitive advantage The Ultimate WMS Checklist: Find the Perfect Fit Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources

{kind=link}

{kind=link}