Transportation Best Practices: Carriers use “game theory” to gain strategic advantage

Ocean cargo carriers vying for market share and sustainable profits are using a variety of methods to get the upper hand this year. Analysts say that while some are leveraging partnerships, others are wagering on reliability to trump that play. Shippers, meanwhile, are hoping that it will all amount to more than just zero-sum.

Latest Logistics News

32nd Annual Study of Logistics and Transportation Trends: Navigating a shallow pool of resources Transportation Best Practices/Trends: Private fleet growth soars Cold Chain: Despite challenges, continues to evolve Freight Audit and Payment Update: Take what you need 2018 Ocean Cargo Roundtable: Unsettled seas More Transportation Trends

Can the current pricing and service behavior of the dysfunctional families comprising today’s leading ocean cargo carriers be explained by game theory? Many industry analysts believe it’s a safe bet.

“Game theory is a tool used to analyze strategic behavior by taking into account how participants expect others to behave,” explains Jock O’Connell, international trade advisor at Beacon Economics. “And because it’s used to understand the behavior of companies in an oligopoly—similar to the carrier alliances in various trade lanes—that certainly seems to apply.”

Game theory is also used to find the optimal outcome from a set of choices by analyzing the costs and benefits to each independent party as they compete with each other. “The Cournot Duopoly and Stackleberg Solutions are examples of game theory that apply here,” says Walter Kemmsies, Ph.D. and chief economist for the engineering firm Moffat & Nichol. “I am a game theorist and agree that this is a legitimate suggestion.”

Economic punditry notwithstanding, industry watchers observe that “brand differentiation” is eroding as other trends are becoming more apparent. For example, rates remain stagnant as vessels are getting bigger and spending more time in ports. Service levels are increasingly unreliable, and shippers are mitigating risk by booking cargo on a variety of deployment schedules.

Alliance trends

On a positive note, however, logistics managers may soon see more collaboration in carrier/terminal relationships designed to enhance throughput and distribution. Shared platforms for information technology will be key for carriers, analysts agree. Since managing excess capacity remains the largest challenge for vessel operators, this trend is especially welcome.

“The container market is currently characterized by ultra-large container ships and orders for mega-vessels in the 18,000-20,000 twenty-foot equivalent range,” says Philip Damas, director of the London-based consultancy Drewry Supply Chain Advisors.

He adds that carriers will need to have ultra-large vessels, be part of an alliance, or participate in a vessel sharing agreement with a partner that has ultra-large container vessels (ULCVs).

Currently, 16 container lines are consolidating their routes and services that essentially control 95 percent of the cargo volumes moving in the major east-west trades. Most recently, Maersk Line and Mediterranean Shipping Co. introduced the 2M Alliance with the 22 joint strings deployed on east-west routes.

Meanwhile, the Ocean Three Alliance—CMA CGM, United Arab Shipping Co. and China Shipping—has commenced five weekly trans-Pacific services, four Asia-Europe routes, four Asia-Mediterranean services, one Asia-U.S. East Coast service via the Suez Canal, and one service dedicated to the Gulf of Mexico.

Even though the two new alliances have teamed to operate the biggest ULCVs in joint services, shippers can opt to use carriers in two smaller alliances. The CKYHE alliance—Evergreen, Cosco, “K” Line, Yang Ming, and Hanjin—represents the third largest player. Coming in a distant fourth is the G6 alliance that includes APL, MOL, Hyundai Merchant Marine, OOCL, NYK Line and Hapag-Lloyd. The G6 has expanded its services in the east-west trades and has pooled its capacity.

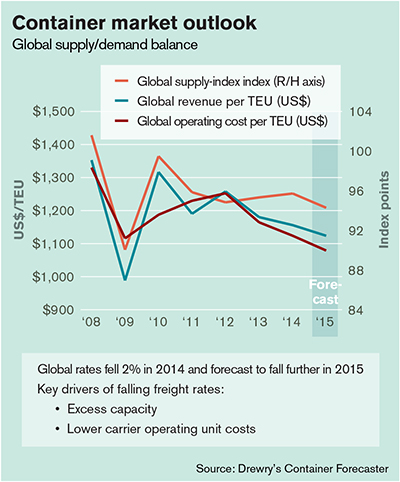

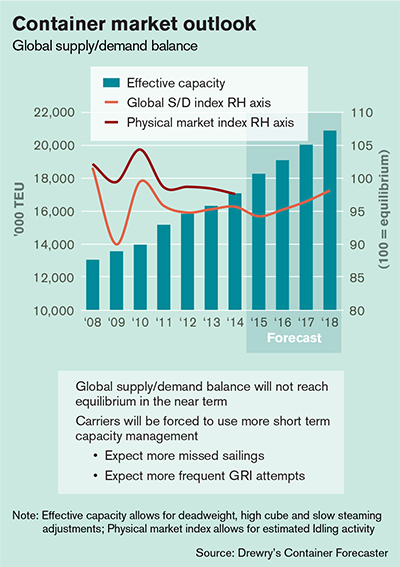

“Yet with all this shifting, the balance of global supply and demand will not reach equilibrium in the near future,” says Damas. “Carriers will be forced to use more short term capacity management, resulting in more missed sailings and frequent attempts to impose general rate increases [GRIs].”

Trans-Pacific trade

The first sign of this rate-hike behavior was evident this month when TransPacific Stabilization Agreement (TSA) carriers recommended a GRI of $600 per 40-foot container increase in rates across the board.

“The trans-Pacific freight market is maturing,” says TSA executive administrator Brian Conrad. “We should not continue to measure it against double-digit annual growth seen a decade ago, but rather in the context of a healthy, steadily improving trade.” He adds that, similarly, the excess vessel supply reported globally is often overstated in the trans-Pacific because it does not take into account infrastructure and other operational constraints.

“The primary imbalance in the trans-Pacific is not so much one of supply versus demand,” Conrad says, “but rather one of costs versus revenue, that in turn drives service.”

Container lines are also forecasting significant increases in shore-side and inland rail, truck, and equipment management costs during 2015 and beyond as demand remains strong, cargo and equipment imbalances widen, and as locomotive, truck, and equipment shortages in key locations push up rates. These conditions reflect long-term operational challenges separate from the prolonged labor problems that have made some carriers reconfigure their deployments away from the U.S. West Coast.

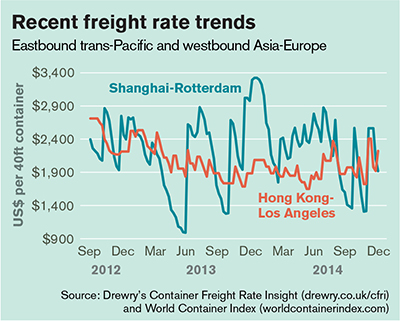

However, carriers can offer no promise of increased reliability. In fact, the latest data shows that the aggregate on-time performance for the trans-Pacific, Asia-Europe, and trans-Atlantic trades dropped to 58 percent in 2015 down from 64 percent year-to-date, according to Drewry.

“The slower-demand winter season should ease some of the congestion pressures and allow for improvement in container shipping reliability,” says Simon Heaney, senior manager of supply chain research at Drewry. “Falling bunker prices should also help raise the on-time performance as carriers will face a lower fuel bill for speeding up ships that fall behind schedule.”

However, the introduction of new alliance service networks in 2015 is a short-term tactic as new schedules are phased in, says Heaney, who adds that “risk-to-reliability” is a classic game theory gambit. “From a shipper’s perspective, it’s good to have a broad portfolio of carriers to pick from,” he says.

Technological fix

With 69 new ULCVs set to join the container fleet throughout 2015, the re-allocation of ships from Asia-Europe to other routes—called “cascading”—will result in problems for logistics managers, say analysts at SeaIntel Maritime, a market intelligence firm based in Copenhagen. With this, global ports and marine terminals will also face new challenges.

“Efficiency standards have declined as vessels spend more time in anchorage, forcing carriers to use their assets in a less optimal manner,” says Lars Jensen, partner and CEO of SeaIntel.

Numerous technology providers are also seeking a fix for this, although industry analysts say it may be both capital and time intensive. “Mega vessels are a very real challenge for the industry,” observes Andy Barrons, senior vice president for terminal technology provider Navis Corp. “Terminals and carriers will have to collaborate at an unprecedented level to manage these massive ships. And if that doesn’t happen, berth productivity will take a hit, vessel load and discharge will be slowed, and shippers will have to alter their long term strategies.”

The answer, says Barrons, is for carriers to match terminal investment in new information technologies and highly skilled workers. “Shippers are concerned about predictability and the speed of moving goods from the terminal to their next destination. In this case, ‘optimal terminal operations’ means moving containers onto rail or trucks in a timely fashion and achieving consistency of the throughput of goods to help shippers forecast and plan their supply chain more accurately.”

Prior to coming to Navis, Barrons worked for INTRAA, a SaaS company linking carriers to shippers. He continues to be an evangelist for collaboration among all industry stakeholders, though not particularly in the game theory context. “Technology is the ‘game changer,’” he insists. “It addresses the communication flow in a maritime world constantly under pressure.”

Article Topics

Transportation Trends News & Resources

32nd Annual Study of Logistics and Transportation Trends: Navigating a shallow pool of resources Transportation Best Practices/Trends: Private fleet growth soars Cold Chain: Despite challenges, continues to evolve Freight Audit and Payment Update: Take what you need 2018 Ocean Cargo Roundtable: Unsettled seas Trucking Regulations: Washington U-Turns; States put hammer down Transportation Trends and Best Practices: The Battle for the Last Mile More Transportation TrendsLatest in Logistics

Descartes announces acquisition of Dublin, Ireland-based Aerospace Software Developments Amid ongoing unexpected events, supply chains continue to readjust and adapt Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources