Special Report: Top 20 3PL Warehouses, 2013

Following a post-recession bump, third-party logistics providers’ warehousing is on track for more modest growth in 2013.

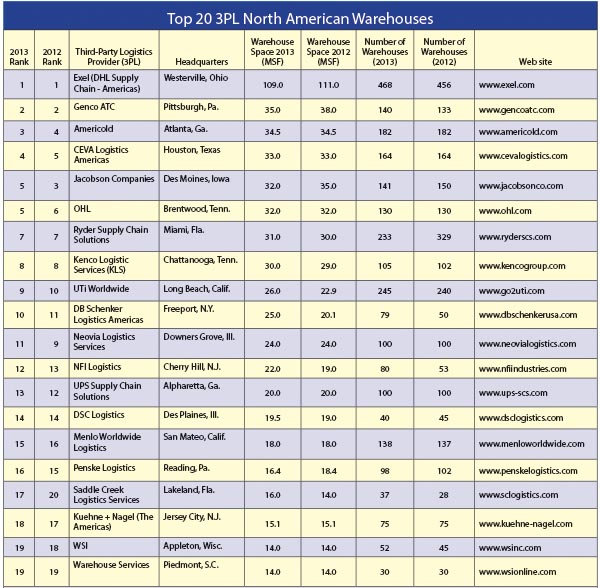

Each year, Modern takes a look at the Top 20 third-party logistics (3PL) warehouses to see who’s leading the way in regard to total square footage of storage space. This year’s annual ranking again reflects the general state of the economy, with slow and steady growth continuing despite economic uncertainties at home and abroad.

“Most of the market is stumbling along as the economy stumbles along,” says Dick Armstrong, chair of Armstrong and Associates, a consulting firm specializing in logistics outsourcing and that partners with Modern for this report. “In general, there’s still not much resurgence in the building of new warehouses or the creation of additional warehousing space.”

Armstrong estimates 3PL warehousing gross revenues for 2013 will grow by about 6% as predicted last year. This follows similar growth in 2012 and stronger growth of 8.2% in 2011. In terms of overall square footage, a 3.6% increase from 547 million square feet to 566 million square feet is within the margin of error given minor variations in reports submitted by companies from year to year. The total square footage for the Top 10 companies, which account for 68% of the Top 20’s total with 387.5 million square feet, is virtually identical to last year’s figures. Read last year’s Top 20 Warehouses report.

Changes in the number of warehouses are also due to the complexities of verifying reports received from each company. Rather than include forwarding locations, transportation logistics, or 20,000-square-foot warehouses, Armstrong says he works to ensure the list focuses specifically on warehousing facilities of 100,000 square feet or more.

Just as warehousing space has remained relatively unchanged since last year, the political and economic climate is also largely the same. Last year at this time, Armstrong feared the fiscal cliff and the possibility of a global recession could make for a challenging year ahead. Twelve months later, Washington continues to fuel uncertainty as economic conditions around the world remain in flux.

“If the people in Washington can do some things for the long-term benefit of the economy, we’ll get some confidence back and that could generate some very interesting things like an increase in nearshoring,” Armstrong says. “BRIC economies are expanding but very burdened by protectionism, which makes it challenging on a global level. China will be looking inward, India is a mess, and Brazil has some real problems to work on. They will not likely contribute to any of the global problems. The Eurozone needs to get out of recession and the United States needs to see some gross domestic product (GDP) improvement. At that time we will see more spending, growing inventories and more warehousing.”

In the meantime, Armstrong says global trade, not GDP, will tend to track closely with 3PL revenue growth. His prediction for 2013 3PL market revenue growth of 6% gross, 4% net, could see the total 3PL market increase to $148.4 billion from $141.8 billion in 2012. “If global trade goes up 3%,” he says, “you can expect 3PLs to post two and a half to three times that.”

The Top 10

With just a few million square feet separating most of them, the positions of the Top 10 warehousing companies have been shuffled a bit this year. Armstrong says that many clients are in six-month contracts and since 3PLs “win some contracts and lose others, you can expect some movement.”

Exel remains firmly in the No. 1 position, with nearly three times the square footage of second-place finisher Genco. “Companies like Genco will continue to move along the path to success,” says Armstrong. “They have a good set of customers and do a good job of caring for them. They will not get burned by excess inventory and are good at reverse logistics.”

Jumping up one spot to third place is Americold, whose footprint has remained unchanged in three years at 34.5 million square feet. Similarly, fourth-place CEVA Logistics Americas has held firm at 33 million square feet, while last year’s third-ranked Jacobson Companies slid to fifth with 32 million square feet, down from 35 million in 2012 and 2011. Armstrong says Jacobson’s decrease in facilities and space is simply due to the elimination of reported values for international transportation management facilities.

Tied for fifth with 32 million square feet is OHL, followed closely by Ryder Supply Chain Solutions with 31 million square feet, up 1 million square feet over Ryder’s reported figures for 2011 and 2012. Kenco Logistics Services also tacked on a million square feet to hold eighth place with 30 million.

UTi Worldwide added more than 3 million square feet to finish ninth at 26 million, while 10th place DB Schenker grew nearly 25% to 25 million. The performances of Uti and DB Schenker were enough to bump last year’s ninth-ranked Neovia Logistics out of the Top 10, despite the fact that Neovia again reported 24 million square feet.

“DB Schenker decided at the corporate level to put some emphasis on contract warehousing in the Americas,” Armstrong says. “They’ve done that, have strengthened their contract logistics offerings and will likely continue to grow.”

Trends for 2014

Increased usage of voice and labor management software

The use of labor management software (LMS) and lean logistics practices are already becoming more of a standard operating procedure, according to Armstrong. “That will only continue,” he says. “We’ve come a long way from the public warehousing operations that did a lot of things with paper.”

Although commonly deployed as a stand-alone solution, LMS is increasingly integrated into overall warehouse operations, Armstrong adds. “This is common especially for larger and more sophisticated operations,” he says. “It is enabling more precision in terms of staffing levels for both full-time and part-time or ‘flex’ employees. On average, about two thirds of the staff are permanent employees and the rest are flex. The control granted by an LMS tends to tip the scales toward more flex and fewer permanent positions.”

Armstrong also anticipates the usage and capability of voice-based picking technology will only improve over time. “Real innovators will use voice where they can and that makes a lot of sense,” he says. “We will see a lot of strategic relationships involving these companies and their partners.”

Although voice and LMS solutions are increasingly scalable and accessible to smaller organizations, Armstrong doubts they will do much to level the playing field. “Small players will have more and more pressure all the time to be more competitive, even as voice, software and cloud-based solutions become more affordable.”

The impact of e-commerce and the cold chain

Faced with the juggernaut that is Amazon, the entire 3PL market is being forced to evolve quickly to compete. “Amazon’s business model is to only recoup about half of what they spend on order fulfillment,” says Armstrong. “This puts a lot of pressure on potential players to create business models that make money.”

Armstrong is also interested in the evolution of cold chain capabilities globally. Rapid change surrounds high-value commodities and pharmaceuticals in this arena, as well as the global movement of foodstuffs from places like South America and seafood from Southeast Asia. “The story of those movements and the related warehousing is critical but also mostly short-term,” Armstrong says. “With high-value goods like drugs or perishable foodstuffs, it’s important to keep those items in motion instead of in storage for any length of time.”

Supply chain managers can have a significant impact on inventory and turnover by positioning their infrastructure for success. “We have not seen any lessening of the pressure to turn inventories and move things along,” says Armstrong. “Whether cold or not, products have to be moved very promptly.”

Article Topics

Latest in Logistics

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report XPO opens up three new services acquired through auction of Yellow’s properties and assets More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources