2019 State of Logistics: Rail/Intermodal

Rail freight volumes trending down

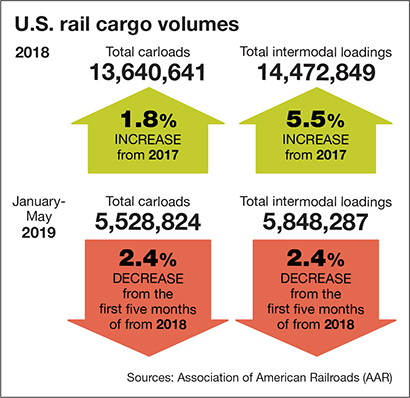

While 2018 was a very strong year for the overall economy, especially when viewed through the lens of demand for goods and services, 2019 is not on the same footing as its predecessor. That appears to be the working thesis when looking at the year-to-date U.S. rail carload and intermodal volumes, based on data from the Association of American Railroads (AAR).

According to the AAR, U.S. carload volumes are down 1.2%, or 66,071 carloads, to 5,528,824, through the first five months of 2019, with the weekly carload average for May down 2.1% annually. This marks the fourth straight month of annual declines.

On the rail intermodal side, the news is also less than encouraging, with annual year-to-date container and trailer volume down 2.4%, or 145,245 units, to 5,848,287. Average weekly intermodal volume for May came in at 263,137, down 5.9% annually, which is also down for the fourth consecutive month.

While the AAR’s year-to-date volume numbers may not be on the same level as previous years, it helps to remember that some caveats come with that premise, according to John Gray, AAR senior vice president of policy and economics.

“Looking at intermodal, we’ve seen records going back to 2013 for every year except for 2016,” said Gray. “Intermodal has been very healthy, and the underlying growth has been largely focused over that time on the domestic intermodal business. International has been much slower, but began to pick up a bit, and I think what we’re seeing this year is another correction similar to what we had in late 2015 and early 2016.”

However, Gray adds that there could be substantial growth in intermodal going forward. “But, like the stock market, there are some troubling things out there such as uncertainty in the economy and if—or when—a correction may be coming.”

On the carload side, Gray says that with carload volumes being more focused on “basic goods,” volumes don’t necessarily mirror the state of the economy.

On the carload side, Gray says that with carload volumes being more focused on “basic goods,” volumes don’t necessarily mirror the state of the economy.

“If you look at the total economy, what you will hear is GDP coming in at 3.1% for 2018. That’s great for the overall economy, but when you look at the underlying components, things like the goods portion of the economy and the amount of the economy that’s really related to the things we can handle, it appears that the growth on that is more in the 1% to 1.5% range. The goods portion of things is what we focus on, rather than the total economy.”

Read the feature article on the 2019 State of Logistics here.

Article Topics

Rail & Intermodal News & Resources

Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report U.S. rail carload and intermodal volumes are mixed, for week ending April 6, reports AAR LM Podcast Series: Examining the freight railroad and intermodal markets with Tony Hatch Norfolk Southern announces preliminary $600 million agreement focused on settling East Palestine derailment lawsuit Railway Supply Institute files petition with Surface Transportation Board over looming ‘boxcar cliff’ U.S. March rail carload and intermodal volumes are mixed, reports AAR Federal Railroad Administration issues final rule on train crew size safety requirements More Rail & IntermodalLatest in Logistics

Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Warehouse/DC Automation & Technology: Time to gain a competitive advantage The Ultimate WMS Checklist: Find the Perfect Fit Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources