2020 State of Logistics: Rail Freight and Intermodal

Rail Freight and Intermodal volumes bearing the brunt of COVID-19 pandemic

Like all modes of freight transportation, the freight railroad and intermodal sectors are not operating in normal times. The ongoing impact of the COVID-19 pandemic serves as the main driver for this, and it’s reflected in year-to-date U.S. rail carload and intermodal volumes in data from the Association of American Railroads (AAR).

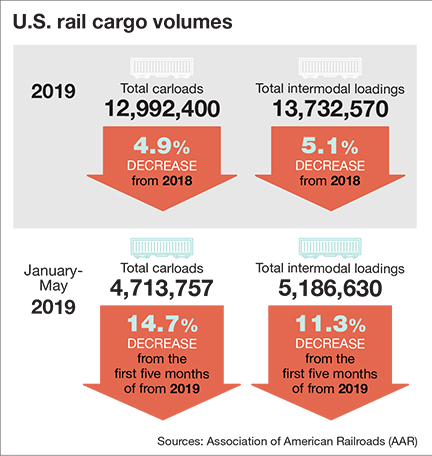

According to the AAR, U.S. carload volumes—at 4,713,757—are down 14.7%, or 815,413 carloads, through the first five months of 2020 on an annual basis with the weekly carload average for May—at 185,043—the lowest ever recorded since AAR began tracking this data in 1989. The numbers have been down each month to date in 2020. What’s more, total U.S. carloads in May were down 27.7% annually, marking the largest monthly percentage decline, as per AAR data.

While they are above carload levels, rail intermodal volumes are also feeling the pain of COVID-19 as well. Intermodal container and trailer volume in May—at 912,922—are down 13% annually. And on a year-to-date basis, intermodal units—at 5,186,630—are down 661,703 units, or 11.3% annually. Average U.S. weekly intermodal volume for May came in at 228,231, for a 13% annual decline and have also been down for each month in 2020 through May.

While they are above carload levels, rail intermodal volumes are also feeling the pain of COVID-19 as well. Intermodal container and trailer volume in May—at 912,922—are down 13% annually. And on a year-to-date basis, intermodal units—at 5,186,630—are down 661,703 units, or 11.3% annually. Average U.S. weekly intermodal volume for May came in at 228,231, for a 13% annual decline and have also been down for each month in 2020 through May.

Addressing the state of rail and intermodal volumes in its monthly “Rail Time Indicators” report, AAR stated that huge swaths of the U.S. and global economies remained shut in May and the impact on rail traffic was predictable.

While U.S. rail carload and intermodal volumes remain low, AAR senior vice president John Gray noted that for the week ending May 30, with the re-opening of the U.S. economy underway, there were gains in 11 of the 20 carload commodities tracked by the AAR. He added that several major commodity areas were improving their showing compared to 2019 in terms of current loading rates to those that had been seen in the prior four-week period.

With COVID-19 dramatically flipping the script for railroad carriers, Tony Hatch, president of New York-based ABH Consulting, said that the industry started 2020 feeling pretty optimistic.

“The railroads entered this year in excellent financial condition and with high hopes it would turn the volume story around by the second half of the year,” says Hatch, adding that the industry’s efforts to change its operating performance under precision scheduled railroading (PSR) had taken fruit, and they thought the economic conditions were right.

“So, the general consensus among the leadership of the railroad industry was that it would be sort of a flat-ish first half of the year and some real growth in the second half of the year,” says Hatch, “with the full-year being a slight uptick, which would be a great turn from 2019, and the industry would enter 2021 with a real tailwind. Of course, that is not how it panned out.”

Article Topics

Rail & Intermodal News & Resources

Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report U.S. rail carload and intermodal volumes are mixed, for week ending April 6, reports AAR LM Podcast Series: Examining the freight railroad and intermodal markets with Tony Hatch Norfolk Southern announces preliminary $600 million agreement focused on settling East Palestine derailment lawsuit Railway Supply Institute files petition with Surface Transportation Board over looming ‘boxcar cliff’ U.S. March rail carload and intermodal volumes are mixed, reports AAR Federal Railroad Administration issues final rule on train crew size safety requirements More Rail & IntermodalLatest in Logistics

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Warehouse/DC Automation & Technology: Time to gain a competitive advantage The Ultimate WMS Checklist: Find the Perfect Fit Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources