25th Annual State of Logistics: It’s complicated

Rollercoaster demand levels and uneven freight volumes in 2013 created havoc in one of the more complicated years on record. In 2014, shippers will need to manage with all the savvy and experience that they can muster to get the capacity they need at a rate that’s fair.

Latest Logistics News

32nd Annual Study of Logistics and Transportation Trends: Navigating a shallow pool of resources Transportation Best Practices/Trends: Private fleet growth soars Cold Chain: Despite challenges, continues to evolve Freight Audit and Payment Update: Take what you need 2018 Ocean Cargo Roundtable: Unsettled seas More Transportation Trends

The state of logistics is complicated. Wearisome logisticians struggled with uneven 2013 freight demand levels and are now bracing for a capacity crisis that is becoming “more severe,” according to the findings of the 25th Annual State of Logistics Report released late last month.

The highly anticipated report, compiled by analyst Rosalyn Wilson and sponsored by Penske Logistics and the Council of Supply Chain Management Professionals (CSCMP), describes last year’s logistics environment as “uneven.” After a slow start to 2013, mid-year shipments were strong before a very deep dive at the end of the year—with not much movement in freight rates across the modes.

However, the picture appears much brighter this year, with Wilson predicting 2014 to be “the best year in the past eight for freight transportation providers.” So far in the first five months of this year, freight shipments are up 13.1 percent year-over-year and payments are up 13 percent. For shippers, they’re seeing higher rates and capacity problems looming.

“The first five months of 2014 have been the strongest freight performance since the end of the Great Recession,” says Wilson. “I believe 2014 will be a banner year for the logistics industry.”

That would be welcome news if not for the whiplash effect it’s having on logistics management professionals as well as the transportation providers who are trying to balance their available capacity with uneven surges in demand.

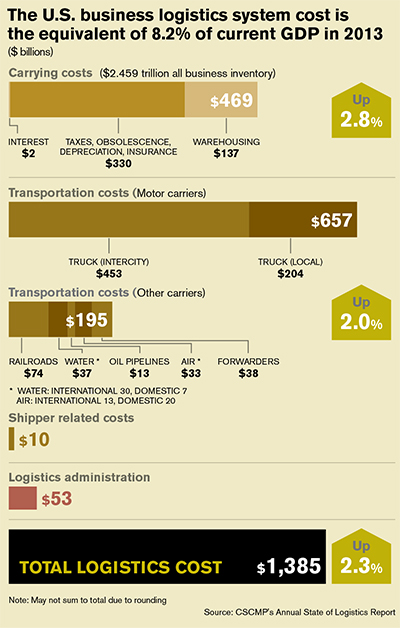

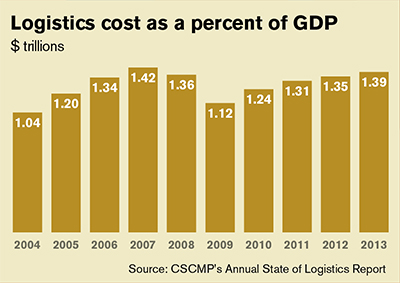

And while the reality for logistics managers feels more like a rollercoaster ride, the report’s raw numbers show the magnitude and importance of the U.S. logistics sector. Last year, U.S. business logistics costs rose to $1.39 trillion, slightly below the peak year of 2007 before the Great Recession. The $1.39 trillion spent last year was a 2.3 percent increase over 2012; however, that percentage gain was a significant drop from the 3.4 percent rise in 2012, according to the report.

Business logistics costs as a percent of the nominal Gross Domestic Product (GDP) declined to 8.2 percent, a tick below the 8.3 percent in 2012. This means that the freight logistics sector was growing at a slightly slower rate than GDP. Those figures compare very favorably to 1981, the first year after trucking was economically deregulated, when logistics consumed 15.8 percent of GDP.

The decline in logistics’ percentage of GDP is traced to lower volumes and lower spending on transportation and services. “That is not good for our industry, but it’s becoming normal since the recession,” Wilson said. “There are pockets that have managed to recover, but the entire logistics sector has not.”

Inventory carrying costs and transportation costs rose slightly last year. Inventory carrying costs increased 2.8 percent, while transportation costs were up only 2 percent in due to weaker shipment volumes and a lack of growth in rates.

Modal highlights from the State of Logistics Report include:

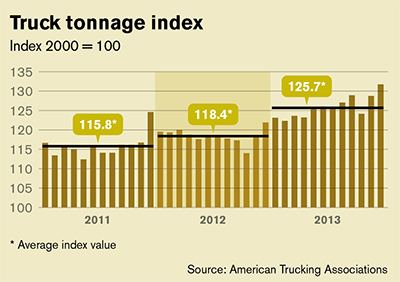

Trucking, the largest component of transport costs, rose just 1.6 percent in 2013, which Wilson called “one of the weakest revenue years in recent history.” That was despite a 6.1 percent rise in truck tonnage.

Rail transport costs rose 4.9 percent in 2013, with Class 1 freight revenue per ton-mile rising 5.3 percent. Overall rail traffic was up 9.2 percent.

Cost of water transport rose 4.5 percent, reversing the previous year’s downward slide. Ocean carriage is “slowly improving” despite additional capacity.

- Airfreight revenue was unchanged in 2013, even though overall revenue tons carried by air fell 0.7 percent.

It’s still the economy

President Bill Clinton based two successful presidential campaigns on a simple slogan: “It’s the economy, stupid.” The same should be said for logistics managers, whose day-to-day activities are closely tied to the current overall economic climate that can be described as lackluster, complicated, and uneven.

“Last year was a much more complicated year from a purely economic point of view,” said Wilson during the release of the report on June 17 at the National Press Club in Washington, D.C. “It was not a stellar year for the economy, but freight did not always mirror the economy.”

Wilson described 2013 as a “roller-coaster.” After a very slow start, there was strong mid-year demand. But just as logistics managers got used to that, demand levels fell off into void with what Wilson termed a “deep dive” by year’s end.

“If the year were to be looked at as individual quarters there were definitely some high points for the freight sector, but also some deep valleys,” said Wilson. “Freight shipment volume experienced five three-year lows during 2013, while freight payments hit three-year highs in eight of the 12 months.”

Freight volume in tonnage terms rose in 2013 more than the number of shipments and revenue figures suggest, but rates remained “stubbornly flat,” Wilson added. This left the trucking industry in a weaker position in 2013. In fact, the rising costs for drivers, equipment, and maintenance pushed marginal trucking companies over the edge, as the number of bankruptcies rose again last year.

Despite a surge in online retail growth, real GDP growth was a paltry 1.9 percent last year compared to 2.8 percent in 2012. That level of sub-par GDP may continue this year. Recently the International Monetary Fund revised its prediction downward to 2 percent from 2.8 percent for GDP growth this year.

However, factors behind this mediocre growth run mostly counter to the growth of freight volume, said Wilson. These included increased inventory investment, a deceleration in imports, and strengthened state and local government spending that were the strongest upward drivers of third quarter GDP.

In the meantime, U.S. exports to China have “dropped off significantly,” Wilson said. That’s because China is in the midst of its own economic problems, she added, noting higher unemployment and falling domestic demand in that country.

Capacity crunch looming

Trucking capacity is becoming a “more severe” issue for shippers, according to Wilson, and the truck driver shortage is currently the top concern for trucking executives who are coping with higher costs for drivers as well as compliance with tougher government regulations.

“More and more drivers are walking away from the industry because of increased regulatory burden and decreased wages,” said Wilson. “In 2012, capacity was tight sporadically throughout the year, and the truck driver shortage is currently having a dampening effect on freight movement.”

Exacerbating the capacity issue is the rising number of trucking bankruptcies. According to panelist Donald Broughton, an analyst at investment banking firm Avondale Partners, trucking bankruptcies increased for seven straight quarters last year and are at a three-year high. Some 21,775 trucks were idled in 2013 due to company shutdowns, which is larger than 2010 and 2011 combined.

Those bankruptcies have continued into this year. Just this month, Delanco, N.J.-based New Century Transportation, a hybrid truckload carrier with 1,300 employees and 2,000 trucks and trailers, closed suddenly, filing for Chapter 7 liquidation. All of this capacity reduction in trucking likely means higher rates for shippers, said Wilson. “And carriers should be able to significantly raise truck rates this year, probably in the 5 percent to 8 percent range.”

That would be a sharp difference from last year, when intercity truck revenue rose 1.8 percent and local delivery revenue was up just 1.2 percent. “Rates have been relatively flat with the exception of spot rates when capacity is scarce,” Wilson said.

Shippers coping

In this complex logistics environment, logistic managers are coping with all of the savvy and experience that they can muster.

Increasingly, they are engaging third-party logistics providers (3PLs) to ensure capacity and handle complicated movements. Although 3PL growth has slowed internationally, domestic transportation management gross revenue was up 7.1 percent, slightly below 2012’s 9.2 percent surge. Dedicated contract carriage grew by 3.6 percent last year, Wilson said, partially because dedicated assures that enough drivers will be available when capacity is tight.

“Human capital is keeping me up at night,” said panelist Mark Althen, president of Penske Logistics, a 3PL that operates a fleet of 2,000 trucks and works with many multinational customers. “If we could find 1,000 to 1,500 drivers we could put them to work immediately. It’s a real strain on capacity.”

Overall, Althen said that he’s witnessed about a 3 percent drop in productivity, mostly because of restraints caused by reduced hours-of-service (HOS) regulations. In the food and beverage sector, Althen said, productivity has dropped as much as 8 percent as the driver squeeze has caused much higher costs.

“Shippers really want to streamline their supply chains, but they want to increase their service levels as well,” Althen said.

Consumers are increasingly expecting next-day or even same-day deliveries; and for some customers, Althen said Penske has arranged specific fleet deliveries to smaller distribution centers in order to speed products to customers.

“We have improved our end-to-end supply chain system,” said panelist John Herzig, vice president of distribution and logistics for Bayer HealthCare’s consumer logistics service center, “We’re now taking additional steps in trimming inventories. We’re reacting quicker to changes, and we’ve re-engineered our entire demand forecasting business.”

Herzig said his supply chain is managing at a “decent pace.” But he said that he had concerns about capacity, HOS, and the driver shortage. To help achieve more efficient capacity, he said that Bayer HealthCare is currently shifting from a major LTL shipper to becoming more of a truckload shipper—and capacity concerns are driving that shift.

“We used to only be concerned about capacity at month-end and quarter end, but now it’s almost a daily occurrence,” said Herzig. “We have to get better at planning, and we have to get better at collaboration with our customers. We have to get better in that space.”

Panelist Richard Jackson, executive vice president of Mast Global Logistics, a subsidiary of Limited Brands Inc., said that his company is “moving through some of the challenges” in moving products with speed and reliability. Even as fashion tastes change faster than ever, he said fashion has been held back because of restrictions in its supply chain.

“There are significant parts of our supply chain that are going slower,” said Jackson, a 16-year veteran of Mast Global Logistics. “The challenge for retail is that we want speed and we need reliability.” To help meet those challenges, Jackson said that he has increased the percentage of freight handled by dedicated contract carriage in order to handle ever-higher demands from fashion retailers.

Specifically, Jackson said that the change in ocean carriage toward slower shipping speeds has caused headaches in his transpacific routes. “We’ve definitely felt the impact in the slowdown in ocean carriage,” he said. “It’s not totally unexpected because ocean carriers have struggled with profitability since the recession.”

That’s translated into higher water rates. Jackson added that over the last 12 months to 18 months he’s seen pressures on rates and also challenges on on-time service.

And this trend most likely will continue across all modes, according to Wilson, as the capacity crunch worsens as freight demand increases. This will only hasten the need for nimble logistics managers who are increasingly asked to juggle more freight demands in a tightening capacity environment and higher costs for nearly every mode.

“All indications are that freight will grow moderately for the rest of the year and the economy should follow suit,” Wilson predicted.

25th Annual State of Logistics Categories

2014 State of Logistics: Less-than-truckload’s welcomed rebound

2014 State of Logistics: Truckload—capacity tight and drivers needed

2014 State of Logistics: Rail rides high

2014 State of Logistics: Ocean is slow and steady

2014 State of Logistics: 3PL—Omni-channel fulfillment to reshape market

2014 State of Logistics: Air’s slight improvement despite headwinds

Article Topics

Transportation Trends News & Resources

32nd Annual Study of Logistics and Transportation Trends: Navigating a shallow pool of resources Transportation Best Practices/Trends: Private fleet growth soars Cold Chain: Despite challenges, continues to evolve Freight Audit and Payment Update: Take what you need 2018 Ocean Cargo Roundtable: Unsettled seas Trucking Regulations: Washington U-Turns; States put hammer down Transportation Trends and Best Practices: The Battle for the Last Mile More Transportation TrendsLatest in Logistics

Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week UPS reports first quarter earnings decline LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources