26th Annual Study of Logistics and Transportation Trends: Transportation at Digital Speed

While a majority of companies strongly agree that transportation is a strategically important function, a significant percentage of them have not organizationally aligned transportation in a manner that supports their goals.

Today’s marketplace rewards those who dare to challenge convention.

Firms like Amazon are departing from traditional business practices, using true supply chain management thinking to blur the boundary between today and tomorrow. In the meantime, we find others standing by the metaphorical shore, not daring to depart to worlds unchartered. In failing to conquer the sea, they fail to see a brighter future.

Fortunately, not all is lost. The findings from the “26th Annual Study of Logistics and Transportation Trends (Masters of Logistics)” suggest that more companies are realizing that new competitors and new business models are shifting customer requirements.

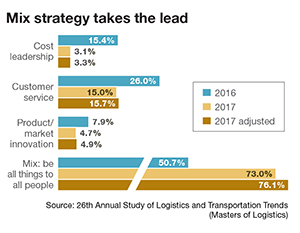

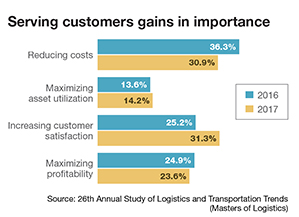

In fact, results from the 2017 study show that roughly 75% of respondents are using the mix strategy (be all things to all people) as the predominant approach for their companies compared to the 51% who we reported utilizing a mix strategy in our 2016 results. However, unlike 2016 where many of these same companies focused on reducing cost as a primary objective, respondents this year were almost equally focused on increasing customer service or reducing costs—31.3% and 30.9%, respectively.

In this year’s study, we examined the relationship between a company’s strategy and its structure. Stated differently, if the strategic direction and the organization’s primary objectives are aligned then it follows that the company will organize itself in a way that enables the achievement of those goals. The results indicate that, for a number of companies, there is a statistically significant gap between their strategic focus and organizational structure.

In this year’s study, we examined the relationship between a company’s strategy and its structure. Stated differently, if the strategic direction and the organization’s primary objectives are aligned then it follows that the company will organize itself in a way that enables the achievement of those goals. The results indicate that, for a number of companies, there is a statistically significant gap between their strategic focus and organizational structure.

For example, companies that reported a cost leadership focus strongly agreed that transportation is strategically important to them. However, there is not this same level of strong agreement for elements that would provide the supporting organizational structure, such as working together with transportation service providers to be successful or spending time with those providers to learn more about various aspects of their business.

In comparison, customer service focused companies are better aligned to support that objective. Firms using a cost leadership strategy tend to view transportation as strategically important, yet in many cases this is not backed up with action. That is, the organizational alignment to support this strategic view is lacking.

Two inferences can possibly be made. First, a successful cost strategy requires a deep understanding of the tradeoffs between cost and service. Second, as service—and particularly speed of delivery—becomes more important in a digital economy, companies along with their transportation service providers must be able to quantify the cost/value of increasing service levels.

“Understanding transportation pricing should rely heavily on data science,” says Tommy Barnes, president of project44, a sponsor of the survey. “Currently, there are a lot of decisions being made without a firm grasp and understanding of how they will affect transportation costs—both in the short-term and long-term.”

In most cases, Barnes contends that transportation providers do not have the right modern technology systems in place to determine the true cost of delivering services to their customers. “Without that, they can’t accurately convey the value associated with increasing service levels or capabilities, leaving their customers to make decisions on a commodity price basis only,” he adds.

Why does this matter? Of the study participants that represented the retail sector, some 54.5% reported that they’re currently working on implementing an omni-channel supply chain structure. While this industry sector is on the front lines on this initiative, they are by no means the only affected group, as the impact of an omni-channel supply chain is being felt by multiple upstream supply chain partners.

Why does this matter? Of the study participants that represented the retail sector, some 54.5% reported that they’re currently working on implementing an omni-channel supply chain structure. While this industry sector is on the front lines on this initiative, they are by no means the only affected group, as the impact of an omni-channel supply chain is being felt by multiple upstream supply chain partners.

The study results show that the top five challenges being faced by companies include (in rank order): 1) supply chain analytics to gain necessary insights; 2) lead time to customers (speed of order fulfillment); tied for 3/4) system wide inventory management and control; 3/4) demand uncertainty across all distribution channels; and 5) cost to serve using an omni-channel approach. Transportation directly influences a company’s ability to meet several of these challenges—most notably the service and cost factors.

Transportation @ digital speed

Some have suggested that what matters to customers will change in a digital economy. The findings of our 2017 annual study suggest “what matters” has indeed shifted, as reflected in the almost indistinguishable top two criteria: price (P) of products and availability (A) of products.

Some have suggested that what matters to customers will change in a digital economy. The findings of our 2017 annual study suggest “what matters” has indeed shifted, as reflected in the almost indistinguishable top two criteria: price (P) of products and availability (A) of products.

This evolution in “order qualifier and order winner,” respectively, is analogous to the merger of the on-time (OT) and in-full (IF) metrics that occurred a few years ago creating a much tougher OTIF performance measure. For e-commerce and omni-channel, P&A is quickly becoming the order qualifier, and the order winner will be determined by speed of delivery.

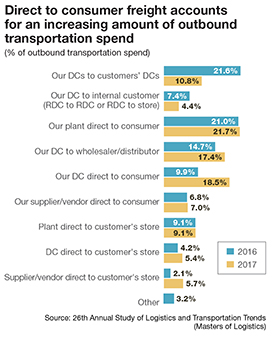

Transportation can be a significant portion of the price of a product through the cost of goods sold, just as it can also make an impact on the speed of order fulfillment. Continuing a trend that we reported in last year’s study, there’s a dramatic shift in the percent of spend for outbound transportation flows direct to consumer from different points in the supply chain.

In 2016, direct to consumer flows accounted for 37.7% of the transportation spend. For 2017 that percentage increased to 46.2 %. We no longer have the option of staying with the current business norms. We have to be “headstrong” and change the way we think about transportation in order to deliver on both dimensions of service and cost.

There is some good news with regard to service. In general, service has improved for over-the-road transportation. Both truckload (TL) and less-than truckload (LTL) posted impressive improvements in on time deliveries and correct invoices.

26th Annual Study of Logistics and Transportation Trends (Masters of Logistics):

By the numbers

For the the 2017 survey, 406 domestic and global logistics, transportation, and supply chain professionals participated, offering insights on trends and issues relevant to today’s busy managers. Participants accounted for an estimated $21 billion in domestic transportation expenditures.

Large companies with annual revenue of more than $3 billion represented 15.6% of the study participants. Medium sized firms, with between $500 million and $3 billion in annual revenue were 18.2% of respondents. The majority of respondents (66.3%) were smaller firms with reported annual revenue less than $500 million.

Respondent companies represent a broad and diverse set of seventeen industry sectors ranging from pharmaceuticals to food. Since the beginning of the study, the core group of participants has been in the manufacturing sector—this year they made up 37.9% of the total.

General manufacturing companies represent the largest sub-sector of that group at 13.3% followed by industrial at 11.4%. Over the past several years we’ve strived to increase the participation of transportation providers in the study in order to more fully understand this perspective. This year that sector comprised 22.2% of all participants, which enabled us to do some comparative group analysis.

According to Barnes this improvement directly results from the adoption of modern automation and visibility tools. “To compete in a digital economy, a company must have real-time visibility into the entire lifecycle of their freight—all the way from quote-to-invoice—in order to manage exceptions, and even prevent errors from happening all together,” he says. “The most efficient way to achieve this is through a multimodal, multiservice connectivity platform, a single source that views and analyzes all inventory and transportation positions.”

However, the results for other metrics were not as rosy. The tightening of capacity in the LTL sector is reflected in a slightly lower equipment availability year-over-year (YOY) as well as a much higher turndown ratio.

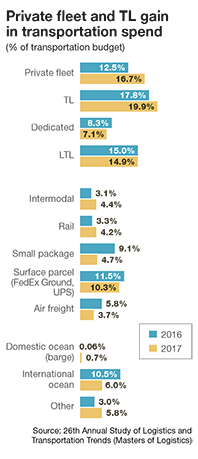

All of this is happening at a time when we’re also seeing some interesting changes in the transportation spend by mode. There was a sizeable increase in spend for private fleet/dedicated (23.8% in 2017 versus 20.8% in 2016). This was the largest shift in transportation modal spend YOY. LTL remained essentially unchanged despite healthy rate increases during the past 12 months. Surprisingly, TL showed a 2.1% increase in its share of the transportation budget despite significant pressure to reduce prices as capacity outpaced demand.

All of this is happening at a time when we’re also seeing some interesting changes in the transportation spend by mode. There was a sizeable increase in spend for private fleet/dedicated (23.8% in 2017 versus 20.8% in 2016). This was the largest shift in transportation modal spend YOY. LTL remained essentially unchanged despite healthy rate increases during the past 12 months. Surprisingly, TL showed a 2.1% increase in its share of the transportation budget despite significant pressure to reduce prices as capacity outpaced demand.

A headstrong approach

A transformation in business has begun. Formerly, firms chose a company-wide strategy based on the assumption that a customer’s decision on whether to purchase a product or service was based primarily on cost. Customers willing to pay more got better service, or more innovative products. Yet, the advent and continual evolution of technology has enabled them to develop a platform where they can deliver goods to the customer over a wider range of costs, as well as service, options.

Customers willing to pay more can get their Kingsford charcoal delivered to their door overnight. If the price point is too high, chose a slower delivery option. A firms’ supply chain capabilities are being transformed by technology, enabling them to serve a much wider set of customers on the cost/service spectrum.

Amazon has approached supply chain management—and transportation specifically—in ways that many competitors would characterize as unfeasible. Despite predictions that what the company is attempting relative to order fulfillment lead times is impossible from a service and cost perspective, Amazon continues to show the art of the possible. This headstrong approach is transforming transportation practice.

Amazon is not the only company adopting a headstrong attitude to developing and implementing service offerings to compete in a digital economy. We believe the future will belong to companies that utilize their supply chains—and principally transportation—to turn the impossible into possible.

Article Topics

Motor Freight News & Resources

Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics XPO opens up three new services acquired through auction of Yellow’s properties and assets More Motor FreightLatest in Logistics

Descartes announces acquisition of Dublin, Ireland-based Aerospace Software Developments Amid ongoing unexpected events, supply chains continue to readjust and adapt Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources