Automation Survey: Uncertainty gives way to growth

In our second automation survey conducted after the pandemic hit, budgets remain solid and the percentage of respondents expecting an increase in equipment and automation spending went up.

As the world continues to adapt to the global Covid-19 pandemic, including sharp growth in e-commerce demand, facilities with distribution and materials handling activities are weighing how quickly to invest in automation and for what processes. Deciding which projects to move forward with in these unusual times, or whether it’s best to keep projects on hold, are decisions DC operators have been weighing since March 2020.

Modern Materials Handling’s “2021 Automation Solutions Study” marks the second automation reader survey we’ve completed since the pandemic’s scale and dangers became apparent. The good news is that budgets remain solid, with an uptick in respondents who expect an increase in automation spending for the coming year.

Since it’s clear that one impact of the pandemic has been a surge in e-commerce, companies with DC operations are likely going to have to continue to layer in more automation to keep up with pressures like tighter order cycle times, and more picking and packing of smaller orders.

Just when the floodgates will really open on automation spending remains to be seen, but our 2021 survey does point to a lower level of uncertainty, with more companies now expecting an increased spend level in the coming year (34% now say it will increase versus 24% last year).

As noted in the white paper “Transformation Age: Shaping Your Future,” published by industry association MHI in mid-2020, the long-term need for automation remains compelling. As the MHI paper puts it: “Businesses, consumers and supply chains will be forever changed by this global pandemic. The organizations that accelerate the implementation of digital, next-generation technologies and solutions to increase their visibility, flexibility and adaptability are the ones that will be best positioned for future success.”

Of the 123 readers who participated in our 2021 automation study, 34% are with companies with less than $10 million in revenues and 18% are with firms that fall into the $10 million to $49.9 million category. The most respondents (59%) are from companies in a manufacturing vertical, 28% are in non-manufacturing sectors like warehousing services, retail or with a third-party logistics provider.

The survey for the “2021 Automation Solutions Study” was conducted in December 2020, but since the previous Automation study was conducted in April 2020 by Peerless Research Group (PRG), this new survey is in effect the 2021 study.

Evaluation priorities

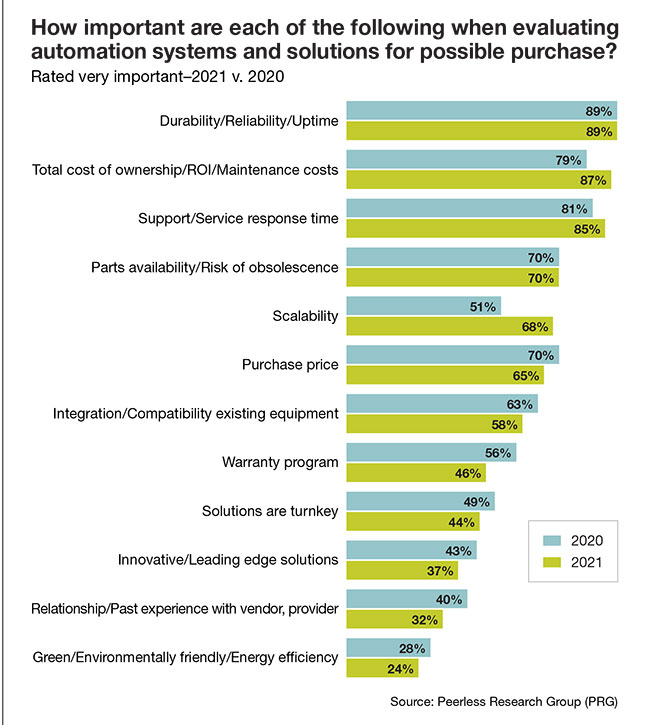

The leading evaluation priorities did not swing wildly, but they did shift slightly versus the 2020 survey. The need for durability and uptime remained the leading driver (89%), which is identical to last year’s percentage.

The leading evaluation priorities did not swing wildly, but they did shift slightly versus the 2020 survey. The need for durability and uptime remained the leading driver (89%), which is identical to last year’s percentage.

This year, total cost of ownership, return on investment (ROI) and maintenance costs came in as the second top driver (87%), up from 79% last year, while support and service response time ranked third (85%).

Additional evaluation concerns include risk of obsolescence and parts availability, and scalability. The priority with the biggest percentage shift was scalability—which drew a 68% this year, up from 51% last year.

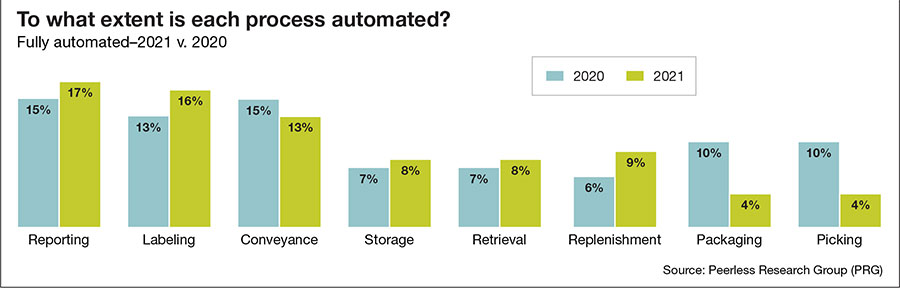

The survey also saw some shifts when it comes to which DC processes are fully automated. For example, reporting is automated for 17% this year, up from 15% last year. Automation of labeling also climbed, from 13% last year to 16% this year.

Conveyors are fully automated for 13% of respondents this year, down slightly from 15% last year, when it was the second-leading, fully automated process. Other changes include slight gains in fully automated storage and retrieval, respectively, among 2021 respondents, though automation of replenishment, packing and picking were down compared to 2020.

In a related question, the survey asked to what extent key processes are automated today, as well as plans to automate each process. For example, while storage is “fully automated” for 8% of respondents, 27% have plans to automate it.

Similarly, picking is now fully automated for 4%, but 24% have plans to automate it, and replenishment is now fully automated for 6%, but 26% have plans to automate it, making it and storage the two processes most frequently cited as moving from manual to automated for 2021.

Pandemic impacts

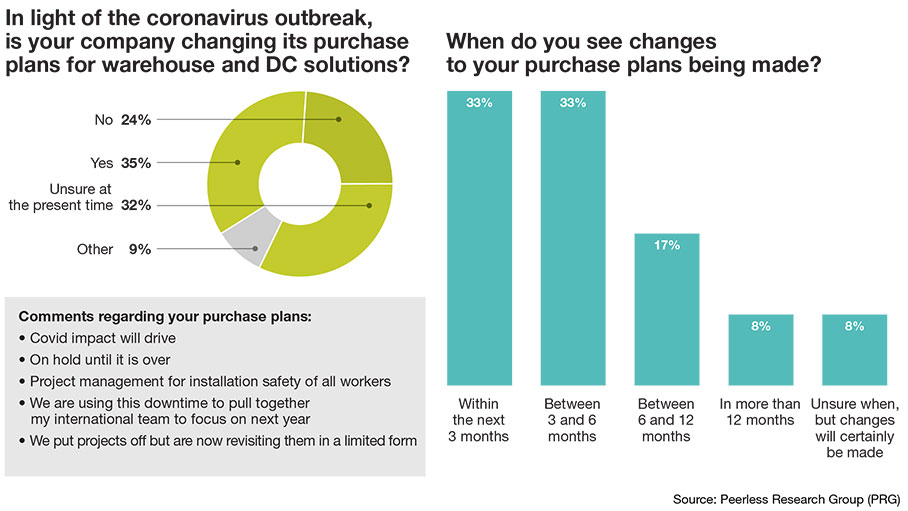

The study asked if the Covid-19 pandemic has changed plans around DC automation. For 2021, 35% said the pandemic has altered purchase plans, 24% said it has not changed their purchase plans, and 32% were “unsure at the present time,” while 9% were “other.” This compares to the previous survey (April 2020), at which time, 21% intended to change their plans, 26% said there were no change of plans, 47% were unsure, and 6% indicated other.

That the “unsure” response was higher early on in the pandemic is not surprising, since in the spring many industries were impacted by the first phase of lockdowns. By the close of 2020 (when the present survey was in the field), the unsure response had dropped, although a higher percentage now indicates that the pandemic had changed their purchase plans.

That the “unsure” response was higher early on in the pandemic is not surprising, since in the spring many industries were impacted by the first phase of lockdowns. By the close of 2020 (when the present survey was in the field), the unsure response had dropped, although a higher percentage now indicates that the pandemic had changed their purchase plans.

Although the percentage of respondents saying the pandemic had changed their plans grew versus earlier in the pandemic (from 21% to 35%), it’s possible some of that change involved companies deciding to move forward with some projects. At the very least, the fact that budgets in this 2021 survey didn’t shrink, and that the percentage expressing uncertainty declined, bodes well for further adoption of automation.

The survey also asked when changes would be made in light of the pandemic. For the 2021 survey, 33% are making changes within three months; another 33% between three to six months, 17% between six and 12 months, 8% beyond 12 months, and 8% unsure. In the previous study, the timing choices were slightly different, with an “immediate” choice that drew a 37% response, 22% expecting changes to purchase plans with the next three months, and 10% between three and six months.

While pandemic-related challenges for DCs certainly continue as of early 2021, these findings suggest many operations may be getting past the point of putting plans on hold. As one respondent put it in the open comments area for this part of the survey, “we put projects off but are now revisiting them in a limited form,” while another commented that special project management procedures had to be adopted for health and safety reasons. That said, another respondent commented that plans were “on hold until it’s over.”

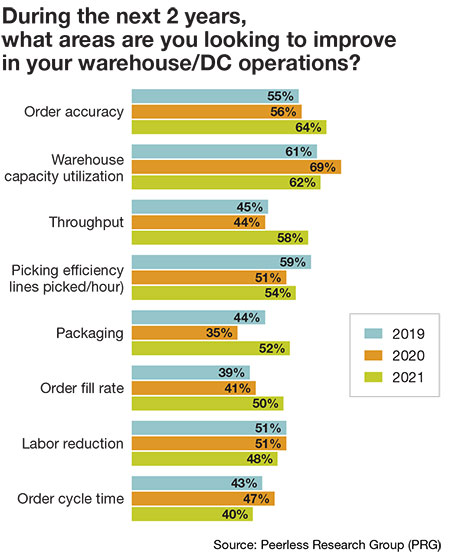

In terms of which operational areas they’d like to improve upon within the next two years, most respondents (64%) named “order accuracy,” up from 56% last year, followed by the 62% who said “warehouse capacity utilization” was the top issue to improve on, and 58% who named “throughput” as the top focus. Last year, capacity utilization was the leading area of focus at 69%, while 44% said throughput, meaning throughput as an area for improvement was up 14%. Making improvements in packaging, throughput and picking efficiency also were on the upswing.

Order fulfillment trends

The survey again confirmed that only a small percentage of respondents consider two of the key order fulfillment processes (picking and packing) as “highly automated” at their sites, though many have a mix of automated and manual processes.

For example, 3% said picking and packing were highly automated (down 2%), though 44% say it’s a mix of automated and manual processes (down from 46% in 2020). With this 2021 survey, 47% of order fulfillment operations are handled mostly or completely manually, up from 45% in 2020.

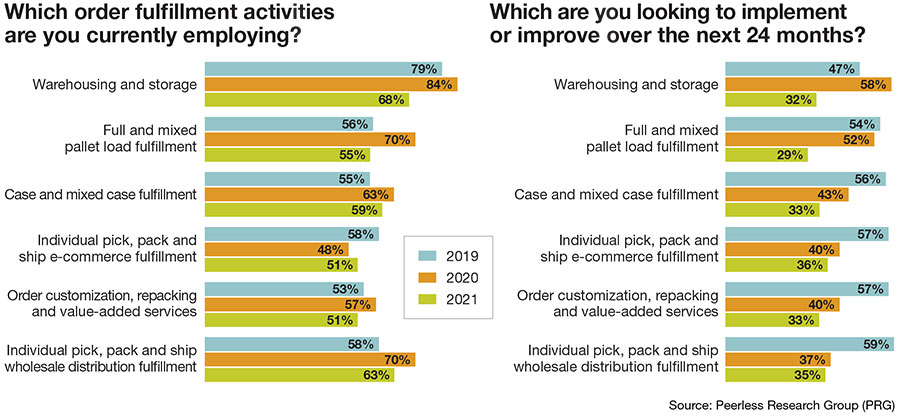

In terms of order fulfillment activities, most companies (68%) currently use warehousing and storage; individual pick, pack and ship for wholesale distribution fulfillment (63%); and full and mixed pallet load fulfillment (55%). Fifty-nine percent are using case and mixed case fulfillment, and 51% are using order customization, repacking and value-added services. Across all these areas, percentage responses for “in use” trended downward among 2021 respondents, though some activities, such as individual pick, pack and ship for wholesale fulfillment, drew a higher response than in 2019.

Over the next 24 months, 36% of companies want to implement or improve current individual pick, pack and ship e-commerce fulfillment activities, and 35% want to improve individual pick, pack and ship for wholesale distribution. Additionally, 33% are most interested in enhancing order customization, repacking and value-added services; 32% will look to improve warehousing and storage operations; and 33% want to improve case and mixed-case fulfillment. Across these processes, the percentages are down from 2020.

Core solutions

Conventional equipment, some of which may have digital elements, is widely used by respondents. For example, 84% said they use lift trucks and rack and shelving, respectively, while dock equipment is used by 70%. Additionally, two-thirds use palletizers, pallets, totes, bins and containers, and 33% currently use hoists, cranes and monorails.

When asked about two-year plans for these categories of conventional equipment, companies are most interested in upgrading or implementing palletizers, pallets, totes, bins and containers (39%), followed closely by lift trucks (37%), and hoists, cranes and monorails (35%). These percentages ran lower than with the 2020 survey.

Robotics going mainstream?

Technologies that leverage robotics such as goods-to-person systems and mobile collaborative robots may not be mainstream yet, but they appear to be getting there.

For example, the 2019 survey found 5% “in use” response for mobile robots, but this year, 16% said mobile robots are in use, down 4% from 2020, but no longer a single-digit percentage. Likewise, shuttle systems and robotic storage and retrieval systems are now in use by 18% of respondents, 2% higher than last year.

The survey also asked about automated storage and retrieval systems (AS/RS) of various types, not necessarily robotic, such as carousels or vertical lifts. These AS/RS solutions currently are in use by 38%, compared to 31% last year. Another choice was goods-to-person picking solutions that deliver totes to a workstation. This category is now in use by 32%, 1% lower than last year’s response.

Automatic guided vehicles (AGVs) are in use by 18% of respondents this year, well below the 34% response from last year’s report, but on par with 2019’s 15% response on current use of AGVs.

Fixed automation equipment such as conveyor and sortation, also are widely used. This year, 50% said they are using automated conveyor/sortation, down from 55% last year. Automated packaging solutions are now in use by 26%, up from 22% last year.

In terms of automated equipment being looked at for implementation or upgrade over the next 24 months, conveyor and sortation systems remain at the top of the respondents’ shopping lists, with 50% saying they have implementation or upgrade plans. This is lower, however, than last year’s 59%.

Across the board, percentages for implementation and upgrade over the next 24 months ran lower than the previous survey, though many categories still drew a response of 30% or higher.

One category that didn’t change much in these 24-month plans is weighing, cubing and dimensioning solutions, on the shopping list for 48% of respondents this year, down 4% from last year. And, 42% also have plans for automated packaging.

Data capture solutions

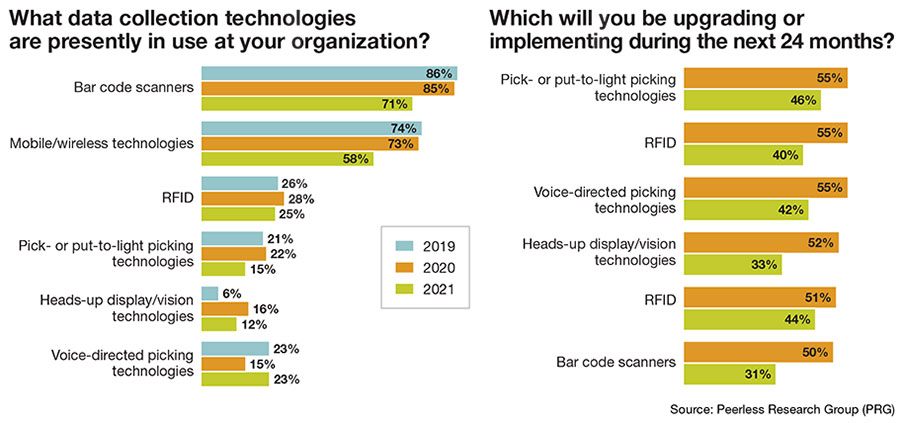

Once again bar code scanners are the type of data collection equipment most commonly used today (71%), though down from last year’s 85%. The only data collection category that saw a rise is “voice-directed” solutions, now used by 23%, up from 15% last year, and equal to the 2019 response.

Also holding fairly steady was use of RFID, used by one-quarter of respondents this year, 3% lower than last year, and 1% down from 2019. Use of heads up displays and vision technologies is in use by 12% of respondents this year, down from 16% last year, but double the percentage from 2019.

Within the next two years, 46% plan to implement or upgrade pick- or put-to-light technology (down from 55% last year). The other most frequently cited categories for upgrade or implementation plans this year are mobile/wireless, named by 44% this year (down from 51% last year), and voice-directed solutions, named by 42% this year (down from 55% last year).

Software trends

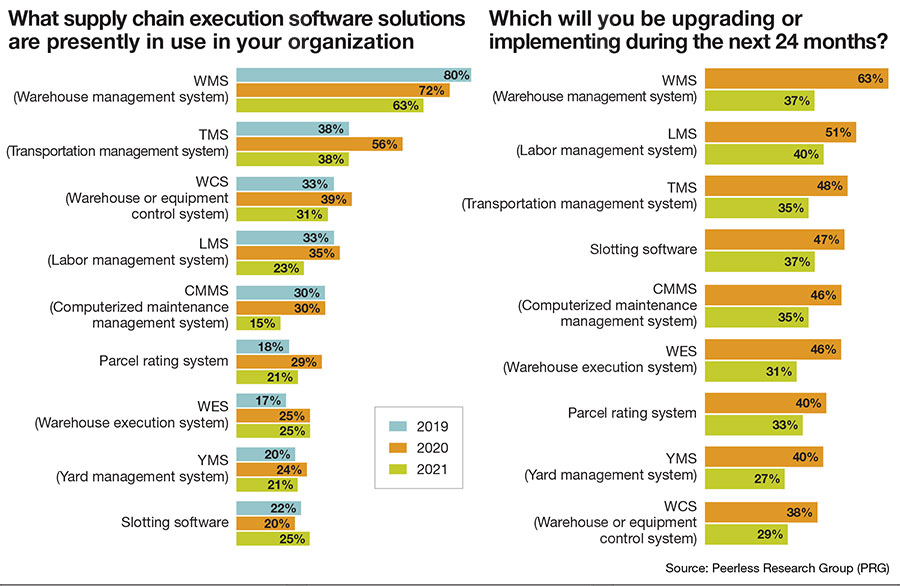

Of the various software categories currently in use, the only category that saw a rise versus the previous survey was slotting, from 20% last year to 25% this year.

Additionally, warehouse execution system (WES) software solutions held steady at 25%. WES is a relatively new solution type that sits between warehouse management system (WMS) and warehouse automation, managing order release, load balancing and the overall flow of work.

Some categories saw an “in use” drop compared to last year, but still equal to or near the 2019 level. For example, this year, current use of transportation management system (TMS) solutions came in at 38%, well below last year’s 56% response, but equal to 2019’s 38% response. Similarly, parcel rating system dropped from 29% last year to 21% this year, but higher than 2019’s 18%

WMS remains the most commonly cited in-use category, used by 63% this year, down from 72% last year. Warehouse control system (WCS) software also drew a smaller percentage this year, though it overlaps WES solutions in some ways, which may explain part of the decline. Of course, every year brings a new pool of respondents with different systems in use and priorities.

Over the next 24 months, 40% plan to implement or upgrade a labor management system (LMS), down from 51% on the previous survey, but still making LMS this year’s top category for implementation or upgrade plans. Last year, that distinction went to WMS, but this year 37% said they had plans for WMS, well below 2020’s 63%.

Across the board, the percentages ran lower this year when it comes to these two-year plans for supply chain execution software projects. The top three this year were LMS, followed closely by WMS and slotting, both at 37%.

When it comes to supply chain and other enterprise software, 66% currently use an enterprise resource planning (ERP) system, down from 70% last year. This year, 57% of respondents use an order management systems (OMS), up by 1%; and 48% use a distributed order management system (DOM), up from 31% last year. The biggest rise this year was for customer relationship management (CRM), up from 55% in last survey to 71% this year.

When it comes to two-year outlook for upgrades or implementations across these supply chain software categories, this year the growth categories were network design and optimization software, with 64% having plans for the category this year (versus 45% last year) and DOM, with 52% having DOM plans versus 36% last year.

Channels & spend outlook

Presently, 60% of respondents purchase their order fulfillment solutions from a distributor/dealer, while 56% buy directly from the manufacturer, and 38% are working with integrators.

In terms of which entities will help with future purchases, distributor/dealer is the most commonly cited source (for 42%) trailed by systems integrators (31%) and direct from OEMs (29%).

When it comes to who handles maintenance, “internal crew” held steady at 69% to remain the most common answer this year. Those having a service contract with a third-party grew from 44% last year to 47% with this survey, while those saying they had a service contract with an OEM declined from 43% to 41%.

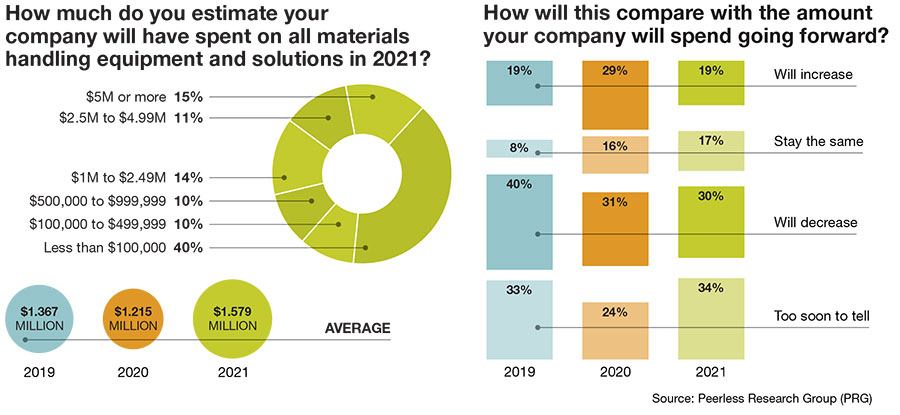

Importantly, the survey found that budgets remain generally strong and close to 2020 findings, with growth in the larger budget brackets. Additionally, the average budget for materials handling equipment and automation came in at $1.57 million, which up from $1.21 million average from last year, and also higher than in 2019.

For 2021, 40% of companies plan to spend less than $100,000 on such solutions, up from 35%. This was offset, however, by growth in the larger spend brackets. This year, 15% of respondents said their company would spend $5 million or more, up from 13%, and 11% indicated spend of between 2.5 million and $4.9 million, up from 4% in this bracket last year.

The survey also asks respondents how next year’s budget will compare with their present budget for equipment and automation. In a positive sign for automation spending, the percentage expecting an increase went up by 10% versus the previous survey (34% now versus 24%) and the “too soon to tell” shrank from 29% last April to 19% this year. However, those expecting some level of decrease in the coming year went up by 1%, from 16% last year to 17% this year.

Interestingly, that 34% of respondents who expect a budget increase for automation and equipment in the coming year is close to what it was in the two surveys that pre-date the pandemic: 2019, when 33% expected their budget to increase in the coming year; and 2018, when 39% expected the budget to rise. That also points to a stronger, longer-term outlook for automation, though it may take until next year’s survey to see what comes to pass and which needs are attracting the most urgency

Article Topics

Latest in Logistics

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report XPO opens up three new services acquired through auction of Yellow’s properties and assets More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources