June truckload and intermodal pricing remains strong, reports Cass and Broughton Capital

Trucking and intermodal pricing levels continue to reap the benefits of a very strong freight environment. That is the main takeaway from the most recent editions of the Truckload Linehaul Index and Intermodal Index from Cass Information Systems and Broughton Capital.

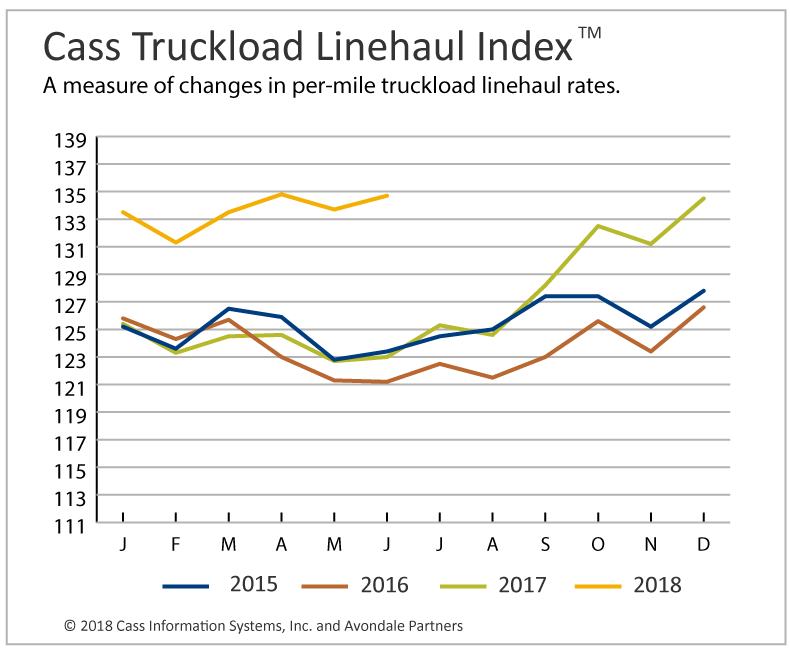

This pricing data is part of the Cass Truckload Linehaul Index and the Cass Intermodal Linehaul Index, which were both created in late 2011. The indices are based on actual freight invoices paid on behalf of Cass clients, which accounts for more than $23 billion annually and uses 2005 as its base month.

According to Cass and Broughton Capital, the truckload index “isolates” the linehaul component of full truckload costs from other components such as fuel and accessorials, which, in turn, provides an accurate reflection of trends in baseline truckload prices.

Truckload rates, which measure linehaul rates, headed up 9.5% in June to 134.7 (the based year is 2005), which is the largest annual gain to date in 2018. Following an industrial recession and being negative for 13 consecutive months from March 2016 through March 2017, the Cass Truckload Linehaul Index has been positive for the last 15 months, with further acceleration intact.

Truckload rates, which measure linehaul rates, headed up 9.5% in June to 134.7 (the based year is 2005), which is the largest annual gain to date in 2018. Following an industrial recession and being negative for 13 consecutive months from March 2016 through March 2017, the Cass Truckload Linehaul Index has been positive for the last 15 months, with further acceleration intact.

“We are increasing our realized contract pricing forecast for 2018 from a range of 6% to 8% to a range of 6% to 12%, and current data is clearly signaling that the risk to our estimate may be to the upside,” stated Donald Broughton, analyst and commentator for the Cass indexes. “We believe that this is the strongest normalized percentage level of truckload pricing achieved since deregulation (normalized meaning except for extreme periods of recovery from recession).”

On the intermodal side, Cass and Broughton reported that total intermodal pricing, or all-in intermodal costs, were up 10.9% in June to 136.7, which represents the largest annual increase going back to August 2011, as well as the 21st consecutive month of increases. The three-month moving average is now up 8.8% annually.

“Tight truckload capacity and higher diesel prices are creating incremental demand and pricing power for domestic intermodal,” stated Broughton. “Longer term, we continue to foresee oil trading in the $45 to $65 range and diesel in the $2.50 to $3.25 range throughout 2018, and higher in certain regions within the U.S.”

“Tight truckload capacity and higher diesel prices are creating incremental demand and pricing power for domestic intermodal,” stated Broughton. “Longer term, we continue to foresee oil trading in the $45 to $65 range and diesel in the $2.50 to $3.25 range throughout 2018, and higher in certain regions within the U.S.”

Article Topics

Rail & Intermodal News & Resources

Four U.S. railroads file challenges against FRA’s two-person crew mandate, says report U.S. rail carload and intermodal volumes are mixed, for week ending April 6, reports AAR LM Podcast Series: Examining the freight railroad and intermodal markets with Tony Hatch Norfolk Southern announces preliminary $600 million agreement focused on settling East Palestine derailment lawsuit Railway Supply Institute files petition with Surface Transportation Board over looming ‘boxcar cliff’ U.S. March rail carload and intermodal volumes are mixed, reports AAR Federal Railroad Administration issues final rule on train crew size safety requirements More Rail & IntermodalLatest in Logistics

DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week UPS reports first quarter earnings declines LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Warehouse/DC Automation & Technology: Time to gain a competitive advantage More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources