Top 25 Freight Forwarders: Top forwarders continue to sail through rough conditions

The push by global forwarders toward purely digital, end-to-end transparency is proving to be crucial amid frequent disruptions that are likely to continue through 2023.

As if 2021 wasn’t bad enough, 2022 is presenting additional layers of disruption to global freight markets with further COVID-related lockdowns, especially in China; Russia’s invasion of Ukraine; exceptionally strong increases in energy prices; heightened competition for talent; and inflation and recession worries that are hitting multiple geographies and supply chains at different locations at different times.

Against this backdrop, buoyant global trade and capacity shortages in ocean and air transport have caused rates to escalate to historic highs.

“These are different challenges than those we experienced in 2020 and 2021,” comments Brian Bourke, chief growth officer at SEKO Logistics. “These are creating even more complexity and volatility in global markets.”

In such a volatile environment, shippers are continuing to lean heavily on their freight forwarders to help bolster their inventories and avoid product stock outs. And at the same time, high freight rates benefited freight forwarders in 2021, as many realized record profits.

“The volatile conditions created growth opportunities for all third-party logistics [3PL] providers, particularly those with strong carrier management, e-commerce, and airfreight forwarding capabilities,” says Evan Armstrong, president of leading 3PL analyst firm Armstrong & Associates (A&A). “Year-over-year, 2021 saw the fastest 3PL growth since we began estimating the market size in 1995.”

A recent report by A&A finds that U.S. 3PL Market gross revenues grew a whopping 48.1% in 2021, bringing the total U.S. 3PL Market to $342.9 billion. It also found that the global freight forwarders with the most gross revenue earnings remained in nearly the same position as A&A’s 2020 report with only slight deviations.

Kuehne + Nagel remained No. 1, whereas DHL Supply Chain & Global Forwarding, which shared that position with K+N last year, moved to No. 2. DSV Panalpina A/S (DSV) came in No. 3 in 2021, down from No. 2 in 2020, while DB Schenker slipped from No. 2 in 2020 to No. 4 in 2021.

Top 25 Global Freight Forwarders*

Ranked by 2021 Gross Logistics Revenue and Freight Forwarding Volumes

| A&A Rank | Provider | Headquarters | Gross Revenue | Air Metric Tons | Ocean TEUs |

| 1 | Kuehne + Nagel | Switzerland | 40,838 | 2,220,000 | 4,613,000 |

| 2 | DHL Supply Chain | Germany | 37,707 | 2,096,000 | 3,142,000 |

| 3 | DSV | Denmark | 28,901 | 1,510,833 | 2,493,951 |

| 4 | DB Schenker | Germany | 27,648 | 1,438,000 | 2,003,000 |

| 5 | Sinotrans | China | 19,097 | 804,000 | 3,940,000 |

| 6 | Expeditors | United States | 16,523 | 1,047,200 | 1,047,725 |

| 7 | C.H. Robinson | United States | 22,356 | 300,000 | 1,500,000 |

| 7 | CEVA Logistics | France | 12,000 | 474,000 | 1,269,000** |

| 7 | Nippon Express | Japan | 18,612 | 971,763 | 747,624 |

| 8 | Kerry Logistics | Hong Kong | 10,516 | 520,415 | 1,229,298 |

| 9 | UPS Supply Chain Solutions | United States | 14,639 | 988,880 | 620,000 |

| 10 | GEODIS | France | 11,900 | 346,667 | 900,866 |

| 11 | Kintetsu World Express | Japan | 9,010 | 728,534 | 715,481 |

| 12 | Hellmann Worldwide Logistics | Germany | 4,718 | 652,100 | 977,500 |

| 13 | Bolloré Logistics | France | 5,701 | 656,000 | 826,000 |

| 14 | CTS International Logistics | China | 3,822 | 416,190 | 1,051,297 |

| 15 | Yusen Logistics | Japan | 7,788 | 410,000 | 742,000 |

| 16 | LX Pantos | South Korea | 6,541 | 142,000 | 1,658,000 |

| 17 | DACHSER | Germany | 8,333 | 365,000 | 530,000** |

| 18 | AWOT Global Logistics Group | China | 4,058 | 486,216 | 250,310 |

| 19 | Logwin | Luxembourg | 2,184 | 182,000 | 715,000 |

| 20 | Hitachi Transport System | Japan | 5,995 | 148,000 | 441,000 |

| 21 | Toll Group | Australia | 6,300 | 117,400 | 523,300 |

| 22 | Worldwide Logistics Group | China | 1,905 | 129,732 | 840,060 |

| 23 | Savino Del Bene | Italy | 3,538 | 88,500 | 660,000 |

| 23 | Maersk Logistics | Denmark | 9,830 | 173,648 | 133,452 |

*Revenues and volumes are company reported or Armstrong & Associates, Inc. estimates. Revenues cover all four 3PL Segments (DTM, ITM, DCC and VAWD) and have been converted to US$ using the annual average exchange rate. Freight forwarders are ranked using a combined overall average based on their individual rankings for gross revenue, ocean TEUs and air metric tons.

**Includes LCL shipments.

Copyright © 2022 Armstrong & Associates, Inc.

C.H. Robinson remained at No. 7 whereas Sinotrans slipped from No. 3 in 2020 to No. 5 in 2021; Nippon Express from No. 5 in 2020 to No. 7 in 2021, and Expeditors from No. 4 in 2020 to No. 6 in 2021. UPS Supply Chain Solutions slipped a notch from No. 8 in 2020 to No. 9 in 2021, and CEVA Logistics slipped from No. 6 in 2020 to No. 7 in 2021, a position in which Armstrong found a three-way statistical tie.

The A&A study also found market segment growth uneven. While gross revenues of dedicated contract carriage (DCC) and value-added warehousing and distribution (VAWD) segments grew 15.3% and 17.0%, respectively, most growth came from international transportation management (ITM) and domestic transportation management (DTM), which increased 74.9% and 52.4% year-over-year respectively.

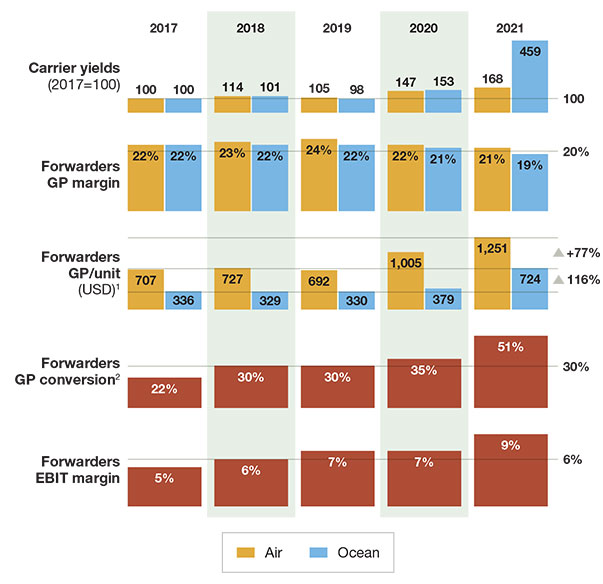

Forwarders earnings are currently elevated, driven by freight rate peaks

Freight forwarders3 performance against market rate developments

1 GP/TEU for ocean, GP/ton for air

2 Defined as EBIT in % of GP

3 Based on average of KN, DSV, expeditors, DGF, Panalpina and Agility

(prior to DSV acquisition)

Source: Clarkson, IATA

ITM, which consists of airfreight and ocean freight forwarding, customs brokerage, and complementary value-added services, led all 3PL segments. To meet demand, service providers in both ITM and DTM increasingly tapped the spot market to source carriers to cover shipments.

The global challenges for providers with a strong focus on freight forwarding are not abating. Nevertheless, they continue to realize impressive profits. In the first half of 2022, Kuehne + Nagel realized a 55% rise in net turnover to roughly U.S. $21.531 billion, EBIT by 112% to approximately U.S. $2.299 billion, and earnings by 113% to around U.S. $1.672 compared to the first half of 2021.

DSV reported that gross profit grew 61% in the first half of 2022 compared to same period in 2021, during which time its airfreight and ocean segments achieved a 105% EBIT increase. Its solutions segment, which includes warehouse, fulfillment, and contract logistics, achieved a 179% EBIT increase.

Merger and acquisition (M&A) activity last year also positioned many forwarders with advantages given their global scale. According to A&A, an astounding 25 large M&A transactions took place in 2021, with purchase prices of more than $100 million. “This is more than eight times the number of large acquisitions made in 1999, when we first started tracking them, and more than three times the number of transactions seen just last year,” says Armstrong.

The most notable was K+N’s purchase of Apex Logistics International for approximately $1.5 billion. “The combination not only made Kuehne + Nagel the largest global airfreight forwarder, handling more than 2.2 million metric air tons in 2021,” adds Armstrong, “but it’s also the largest 3PL globally, replacing DHL Supply Chain and Global Forwarding in both instances, and continues to hold its place as the largest ocean freight forwarder.”

DVS acquired Agility’s Global Integrated Logistics (GIL) in August 2021, which will further contribute to its growth and adding strength to the overall global forwarding services market.

Possible global deceleration

Florian Neuhaus, partner at McKinsey & Company, warns that current conditions point to a deceleration of global market dynamics—at least on the demand side. For one, International Monetary Fund (IMF) projects global trade to slow from an estimated 6.1% in 2021 to 3.6% in 2022 and 2023.

Beyond 2023, the IMF expects growth to fall to about 3.3% over the medium term, which is 0.8 and 0.2 percentage points lower for 2022 and 2023 than projected in January. In addition, the June Manufacturing Purchasing Managers Index (PMI) registered 53%, down 3.1 percentage points from the reading of 56.1% in May.

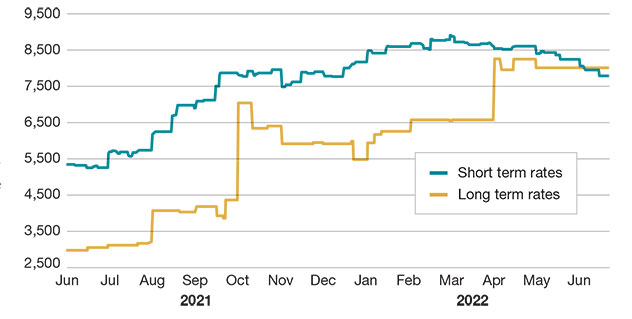

Container freight rates, China to U.S. West Coast, 2021-2022

USD per 40’ dry container

Source: Xeneta.com

“This is the lowest Manufacturing PMI reading since June 2020, when it registered 52.4%,” Neuhaus says. “The New Orders Index reading of 49.2% is 5.9 percentage points lower than the 55.1% recorded in May.”

Neuhaus notes that lower demand is already driving down freight rates. “In ocean, spot rates have fallen below contract rates,” he says. “Airfreight rates have continued to drop since the return of more passenger flights and the introduction of airline’s summer schedules.”

Meanwhile, with demand-side pressure likely to slow over the next 12 months to 24 months, Neuhaus sees shippers taking advantage of declining rates. “Many shippers will go in the market and tender their volumes again,” he says. “At the same time, many shippers will be looking to build stronger partnerships with their

logistics providers in order to build more resilient supply chains.”

Within the next four years to five years, McKinsey expects ocean and airfreight rates to gradually decline from their 2021/2022 peaks, but stay slightly elevated compared to pre-pandemic, as lower constrained supply will prevent a full mean reversion. “As yields decline, so will 3PL earnings that are fundamentally linked to carrier rates,” Neuhaus says.

Unpredictable and competitive

To remain competitive, some global freight forwarders have ensured access to ocean capacity and chartered air freighters amidst belly capacity shortages as well as suggested alternatives to traditional shipping practices.

“This may include considering more extended booking windows of five to six weeks, using new ports, different modes of transportation—including multimodal solutions—and even alternative sourcing decisions,” says Jeff Pearlman, ocean freight senior marketing manager at UPS. “Some of the options defy what we used to consider best practices, for instance: using less-than container load for the most urgent PO’s or partial shipments; limiting the number of containers per bill of lading to one or two so carriers can more easily accept and transport the bookings; and microscopically managing your vendors so the product they ship first is the product you must urgently need.”

Freight forwarders are also upping their competitive position increasingly by focusing on people. “For us, that is Team CEVA,” says Shawn Stewart, regional managing director for North America, CEVA Logistics. “Our diverse team possesses the skills and knowledge to provide solutions across numerous industry verticals. This expertise is combined with strong customer relationships to deliver our central commitment we call Responsive Logistics.”

Going forward, Armstrong sees the true leaders being those that embrace technological innovation and demonstrate strong carrier management skills. “This has allowed freight forwarders to efficiently tap long-standing carrier relationships to cover shipper demand versus being overly reliant on using load boards or traditional means to buy capacity at spot market rates,” he says.

C.H. Robinson has implemented a strategy that leverages technology and innovation—along with people, scale and a global suite of services. Mike Short, C.H. Robinson president, says this gives C.H. Robinson a unique position to serve global shippers’ needs.

“This approach enables us not only to help our customers navigate today’s increasingly complex global supply chains, but also orchestrate comprehensive, integrated strategies in a constantly changing environment,” Short says. “Being nimble was no longer just the smart option for shippers, it became the only option when disruption hit its peak. We continue to utilize our scale and multi-modal model to our customers’ advantage as challenges shift in the industry, which we are seeing now with the softening in demand on the trans-Pacific.”

According to Stewart, CEVA applies industry-leading technology such as WMS, shipment visibility tools, robots, cobots, wearables, electric and autonomous vehicles, or just a simple algorithm that improves how the provider uses its data. “We’re building an innovation culture, and for us, innovation is the implementation of new ideas with business impact,” he says.

Stewart points out how CEVA has the scale to implement supply chain solutions around the world. “That global awareness and the agility to respond to our customers’ needs locally has helped us strengthen our business—and many of our customers—throughout a few very challenging years. The focus on agility will continue to gain importance in the months and years to come.”

According to Neuhaus, this stronger push by global forwarders toward a digital channel and end-to-end transparency has proven to be crucial amid frequent supply chain disruptions that are likely to continue going forward. “Larger forwarders were generally in better position to make these investments in the IT infrastructure that enable both transparency and an improved digital sales experience,” he concludes.

Market drivers for freight forwarders

What are the key trends making an impact on freight forwarders today? Florian Neuhaus, partner at McKinsey & Company, suggests the following.

Sustainably and de-carbonization. Forwarders are actively looking for ways to decarbonize their offerings to satisfy demand from some shipper segments. To move the market and encourage carriers to act, some forwarders are willing to sign volume guarantees. These guarantees enable carriers to hedge some of the investment risk they need to take to decarbonize.

Growth dynamics stemming from e-commerce. More than 50% of global logistics growth will be driven by e-commerce over the next five years. Forwarders need to think about what role they can play in this market—for example, more of a consolidator for cross-border e-commerce volumes that are moved by air.

Changing competitive dynamics and market consolidation. The overall market is becoming more competitive, especially on the ocean freight side. Shipping has become a more consolidated market, and liners are improving their digital direct to customer channel, which allows them to reach a much broader customer base. Therefore, forwarders must find ways to further differentiate their offering and provide additional value to their customers.

Article Topics

Motor Freight News & Resources

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics XPO opens up three new services acquired through auction of Yellow’s properties and assets FTR’s Trucking Conditions Index weakens, due to fuel price gains TD Cowen/AFS Freight presents mixed readings for parcel, LTL, and truckload revenues and rates Preliminary March North America Class 8 net orders see declines National diesel average heads down for first time in three weeks, reports EIA Trucking industry balks at new Biden administration rule on electric trucks: ‘Entirely unachievable’ More Motor FreightLatest in Logistics

LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics Investor expectations continue to influence supply chain decision-making The Next Big Steps in Supply Chain Digitalization Warehouse/DC Automation & Technology: Time to gain a competitive advantage The Ultimate WMS Checklist: Find the Perfect Fit Under-21 driver pilot program a bust with fleets as FMCSA seeks changes Diesel back over $4 a gallon; Mideast tensions, other worries cited More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources