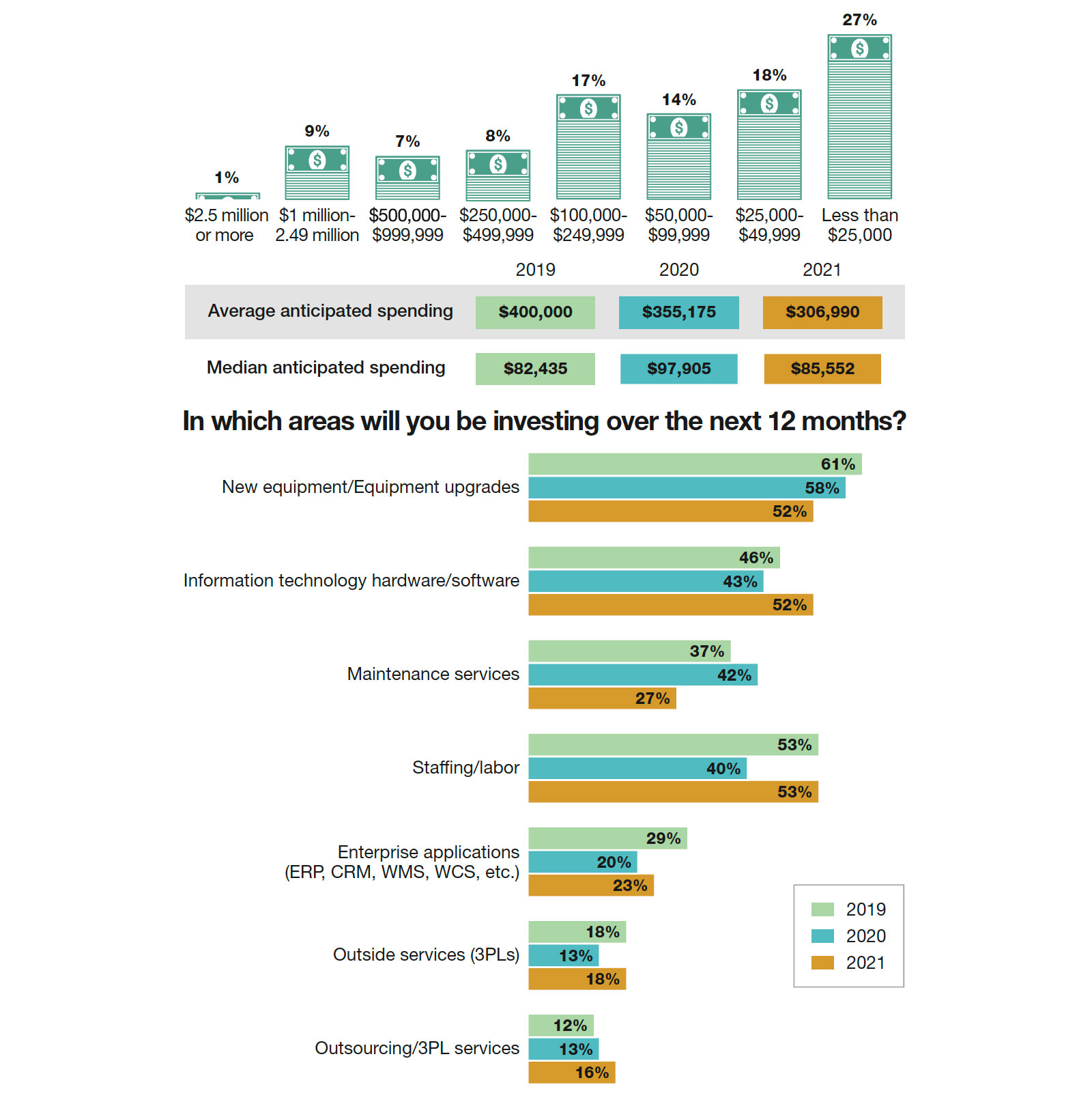

In total, over the next 12 months, approximately how much do you expect to spend on materials handling equipment and information systems solutions?

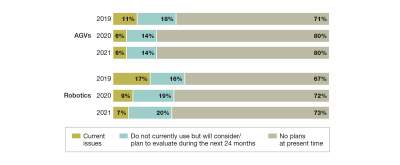

Apart from the survey, the use of robotics by many larger DC operators and 3PLs is growing and even becoming more mainstream. For this respondent mix, interest in robotics and AGVs is at least holding steady. What’s more, it may be that the market is entering a stage in which robotics and AGVs are no longer novelties, but rather another set of options to be used in combination with fixed automation—or with each other.

“Some of these applications for robotics, like palletizing, have been around for a long-time, and AGVs have also been around a very long time, so in that sense, robotics and AGVs are nothing new, but there is a trend toward wanting greater flexibility in automated transport,” explains Derewecki. “There is definitely strong interest in the market in both of these categories as a way of automating various workflows. Some of our clients are also combining AMRs and AGVs with other technologies to create highly automated material flows.”

When it comes to mobile technologies, there weren’t any big shifts compared to last year’s findings, with 53% either using or having plans for mobile solutions, down 2% from last year. This year, 38% said they’re providing more employees with mobile solutions, up from 31% last year.

We also ask about current use and 12-month plans for specific types of mobile devices and bar code scanning and printing equipment. Bar code scanners, for example, are utilized by 55% today, and 40% have plans to deploy scanners during the next 12 months. Similarly, voice-directed technology is used by 28%, and 22% have voice system plans during the next 12 months.