State of Logistics 2013: New order, new opportunities

New state of logistics translates into new opportunities for shrewd managers who can leverage their unique skills and solid transportation relationships into value for their companies.

Latest Logistics News

STB Chairman Martin J. Oberman retires LM reader survey drives home the ongoing rise of U.S.-Mexico cross-border trade and nearshoring activity USPS cites continued progress in fiscal second quarter earnings despite recording another net loss U.S. rail carload and intermodal volumes are mixed, for week ending May 4, reports AAR New Ryder analysis takes a close look at obstacles in converting to electric vehicles More NewsThere’s a “new order” evolving in the logistics and transportation arena, one that’s amplifying the challenge of securing capacity, yet one that will highlight the value of having a shrewd logistician at the helm of a company’s shipping decisions.

Today’s savviest logistics practitioners are driving out costs from the Transportation system and creating new “omni-channel” distribution networks designed to take advantage of customers’ changing buying habits. And to accommodate the ever-finicky consumer, they’re no longer making decisions based on modal “silos.” Instead, shippers are becoming “modal agnostic,” seeking capacity when and where it makes the most economic sense for their operations.

In fact, the results of the Council of Supply Chain Management Professionals’ 24th Annual State of Logistics Report, co-sponsored by Penske Logistics, shows that the sharpest logistics management professionals are saving their companies millions in transport, warehouse, and shipping costs.

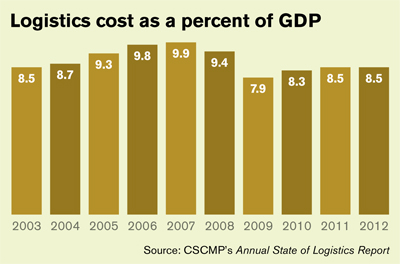

According to the report, logisticians and supply chain professionals have once again driven inefficiencies out of the business transportation system. Last year, business logistics costs stayed steady at 8.5 percent of gross domestic product (GDP), the same level as they were in 2011, the report says. That compares to about 17 percent of GDP back in 1979, the year before trucking was economically deregulation, allowing innovation to flourish.

According to the report, the cost of the U.S. business logistics system rose 3.4 percent in 2012, that’s less than half the increase from 2011 and still short of the peak 2007 level. Total business logistics costs were $1.33 trillion, up $43 billion from 2011.

![]()

2013 State of Logistics categories

- Less than Truckload

- Truckload

- Rail

- Ocean

- Air

![]()

Inventory carrying costs and transportation costs rose “quite modestly” in 2012, according to Rosalyn Wilson, author of the 24th Annual State of Logistics Report. Inventory carrying costs rose 4 percent while transportation costs were up only 3 percent, thanks to weak and inconsistent shipping volumes and strong blowback by shippers for carriers to hold rates.

“Logistics costs as a percentage of GDP in the U.S. compares quite favorably to that of our trading partners,” says Wilson. “Slow economic growth has kept the percentage low, but the supply chain sector has made great strides in productivity, asset utilization, and inventory management in the past three years.” These supply chain management improvements will continue even as higher volumes return to the market place, Wilson predicts.

New normal, new options

Logisticians and supply chain experts have been coping with a new economic paradigm since the Great Recession ended in 2009. This has caused changes in supply chain options as well as other economic realities. Wilson noted that slow growth and lackluster job creation caused the global economy to wallow in mixed levels of recovery.

“You’re probably thinking that there’s not been much to celebrate,” says Wilson. “Perhaps it’s time to ask: Is this the new normal?”

In her presentation, Wilson said that she believes we’re experiencing a “new order” of elements that are translating into a economic paradigm that’s strongly affecting the logistics and supply chain sectors. This “new order” is characterized by slow growth (GDP growth of between 2.5 percent and 4 percent), higher unemployment levels (7.5 percent in the U.S.), and higher reliance on part-time workers during slower job creation.

For logistics managers, this means less predictable and less reliable freight services as volumes rise but capacity does not. In areas such as ocean transport, says Wilson, this can mean slower transit times. “I do believe that the economy and logistics sector will slowly regain sustainable momentum, but we will still experience unevenness in growth rates,” Wilson says.

For cutting-edge logistics managers, however, the current environment also means great opportunities to secure increasingly tight capacity in an era of shrewd rate bargaining. This is partly because the trucking industry, in particular, is facing a lid on capacity due to higher qualification standards for drivers at the same time top carriers are becoming increasingly selective in their choice of customers.

“Truck capacity is still walking a fine line—few shortages, but industry-high utilization rates,” says Wilson. “Qualified truck drivers have become a valuable commodity in very short supply.”

Wilson predicts that driver shortage will exacerbate as the economy improves even further. She’s predicting the current driver shortage of 30,000 will hit 115,000 by 2016. In the ocean and air freight sectors, meanwhile, overcapacity is the issue while the railroads report that they have more than 20 percent of their freight cars in storage.

The following summarizes the performance of individual freight modes according to the 24th Annual State of Logistics Report:

- Trucking rose 2.9 percent. The sector is “just on the breach” of experiencing capacity problems due to higher regulations and lack of fleet growth.

- Rail costs rose 4.9 percent, well below its 16 percent increase in 2011. Class 1 revenue per ton-mile rose 5.3 percent even as ton-miles actually decreased 1 percent in 2012.

- Maritime costs fell 0.9 percent in another disappointing year for ocean carriers. Capacity is expected to rise 10 percent this year, but these new vessels “will be difficult to deploy” without further damaging the industry’s dynamic, the report says.

- Air freight revenue gained 3.1 percent while domestic air cargo ton-miles rose 2 percent, but international fell 3.9 percent. The all-cargo air industry is facing “chronic over-capacity and deteriorating yield,” according to the report.

- Oil pipeline ton-miles were virtually flat last year. But that was “more than offset” by rate increases as pipeline revenue rose 8.3 percent in this heavily economically regulated sector.

Trucking in a “delicate balance”

Trucking, in particular, faces tough challenges in merely getting an adequate supply of drivers. “The trucking sector has been in a delicate balance for several years, just on the breach of experiencing capacity problems,” says Wilson.

The U.S. Department of Labor estimates that truck drivers will account for 43 percent of the growth in logistics jobs in coming years, but Wilson asks: “Where will these drivers come from?”

She says that truck drivers represent a labor category with the fewest potential workers to fill those jobs. Only about 17 percent of the current driver population is under 35, with a larger portion close to retirement age. In the meantime, the government crackdown on unsafe drivers, the industry’s inability to attract younger or minority workers, the high cost of driver training programs, and a revival of the construction industry are all serving to squeeze the available pool of drivers.

According to the report, private fleet owners also have an aging population, and they’ve been attracting some of the most desirable jobs with better pay and working conditions. In comparison, railroads are in “very good shape” regarding infrastructure, equipment, and personnel. Rail infrastructure spending rose 16.1 percent last year, topping $13 billion, yet efficiency rose. Class 1 rails consumed 2.1 percent less fuel last year despite hauling more tonnage in 2012 compared to year-earlier levels.

Shippers are increasingly turning to third-party logistics providers (3PLs) to help with their capacity issues. Revenue in the 3PL sector rose by a healthy 5.9 percent last year, the report said, citing figures from Armstrong and Associates, a leading logistics research and consulting firm.

“The domestic transportation management segment of the 3PL market was the fastest growing, with gross revenue up 9.2 percent,” says Wilson. The service providers’ cost of purchasing transportation has risen “modestly,” she adds, noting that competition in the marketplace is helping hold down rates.

So far this year, freight results are “mixed,” Wilson says. Rail carloads were down 1.7 percent year-over-year, but year-to-date intermodal units rose 4.1 percent for the first five months, compared with the same period last year. The American Trucking Associations’ monthly truck index has risen for three of the first five months, an indication of the up-and-down nature of the freight recovery.

“Slow growth will be with us for the next several years,” Wilson predicts. “Logistics will still be a bumpy road.” However, the forecast of stable or decreasing energy prices is “welcome news” for shippers, Wilson says, adding that fuel has become a “pretty manageable piece” of the logistics puzzle.

Industry reaction to report

Shippers and logisticians reacted to the 24th Annual State of Logistics Report with confidence knowing that there’s adequate capacity for those knowledgeable practitioners willing to do their homework and create long-term relationships with carriers to secure sufficient capacity.

Marc Althen, president of Penske Logistics, a sponsor of the report, said that he’s seeing higher inquiries from shippers looking for 3PLs, especially for transportation management solutions to help manage their freight.

One area that concerns shippers is sufficient availability of truck drivers. Althen says that driver pay must rise to attract and retain drivers. Penske’s annual driver turnover is 17 percent, he says, compared to close to 100 percent for most large truckload carriers.

Brent Beabout, senior vice president of supply chain for Office Depot and former vice president of engineering for DHL Express, says that his current company has increased its use of intermodal and is also using more dedicated trucking options to combat the driver shortage.

“That dedicated fleet has been a good answer for us,” says Beabout. He added that Office Depot co-mingles freight from all three of its distribution channels—in-store retail, business, and online sales—in creating an omni-channel distribution network. He adds that the retailer has started redesigning its freight network to take more advantage of intermodal options.

“All retailers are looking into redesigning their store size and location due to the growth in online business,” says Beabout.

Steven Bobb, executive vice president and chief marketing officer for BNSF Railway, says that there are some segments of economic growth, such as intermodal and energy exploration, but there’s “no sustainable” growth in most of the overall economic sectors.

BNSF is spending $14 billion on capital investment this year, Bobb says. But he adds that the biggest issue is making sure that shippers have adequate capacity in the correct geographic regions to handle the uneven nature of freight today.

Paul Svindland, COO of Pacer International, a major intermodal company that offers truck brokerage and other services, says that cross border intermodal traffic is growing well. “I am cautiously optimistic about the rest of 2013 going into 2014,” he adds. “There is still growth, but probably not as much as saw at the start of 2012.”

However, the July 1 hours-of-service changes will affect regional and long-haul carriers, causing an increase in costs between 5 percent and 9 percent on productivity, says Svindland. Penske’s Althen says that he estimates 3 percent in higher costs, largely because Penske’s average length of haul is much shorter.

Beth Ford, vice president and chief supply chain operations officer for Land O’Lakes, says her company has doubled revenue in the past five years, largely due to exports of agricultural products. “We continue to see optimism in our business going forward,” she says.

So the consensus from shippers in the know is expect higher freight rates as capacity tightens, be prepared to be flexible in modal selection and be aware that carriers are being increasingly choosy with whom they do business in this tighter capacity environment.

In summary, 2012 was “certainly not a great year from an economic perspective,” Wilson adds. While the freight sector continues to improve, prospects for high growth are limited. Wilson simply concludes: “Slow growth will be with us for many years.”

![]()

2013 State of Logistics categories

- Less than Truckload

- Truckload

- Rail

- Ocean

- Air

![]()

Article Topics

Latest in Logistics

STB Chairman Martin J. Oberman retires LM reader survey drives home the ongoing rise of U.S.-Mexico cross-border trade and nearshoring activity A buying guide to outsourcing transportation management SKU vs. Item-level Data Visibility: Why it Matters for End-to-End Traceability Key benefits of being an Amazon Business customer with Business Prime USPS cites continued progress in fiscal second quarter earnings despite recording another net loss U.S. rail carload and intermodal volumes are mixed, for week ending May 4, reports AAR More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Logistics Management

Latest Resources